New York Life Insurance Company Brokerage General Agency Imo

New York Life Insurance Company Brokerage General Agency IMO plays a pivotal role in expanding access to comprehensive insurance and financial solutions across the United States.

As a respected intermediary within the New York Life network, this Independent Marketing Organization (IMO) supports agents and brokers in delivering life insurance, retirement planning, and wealth protection products. By leveraging strategic partnerships, robust training resources, and dedicated administrative support, the IMO enhances distribution efficiency and agent success.

Its alignment with New York Life’s long-standing reputation for financial strength and customer service ensures clients receive reliable, tailored solutions. This agency model fosters growth, professionalism, and client-centered service throughout the insurance marketplace.

Drywall Business Insurance Massachusetts

Drywall Business Insurance MassachusettsNew York Life Insurance Company Brokerage General Agency and IMO Partnerships

New York Life Insurance Company, one of the largest and most respected mutual life insurers in the United States, operates through a comprehensive distribution network that includes its own agents, financial representatives, and strategic partnerships with independent marketing organizations (IMOs) and brokerage general agencies (BGAs).

These affiliations allow New York Life to expand its market reach, especially in the sale of life insurance, annuities, and other financial products, by collaborating with third-party agencies that specialize in agent recruitment, training, and field support. Brokerage General Agencies act as intermediaries between carriers like New York Life and independent agents, while IMOs provide marketing, administrative, and operational infrastructure to help agents sell policies effectively.

By aligning with established IMOs and BGAs, New York Life enhances its ability to serve a broader customer base without compromising underwriting standards or service quality. These partnerships are governed by formal agreements that ensure compliance with regulatory requirements and uphold the company’s long-standing reputation for financial strength and policyholder service.

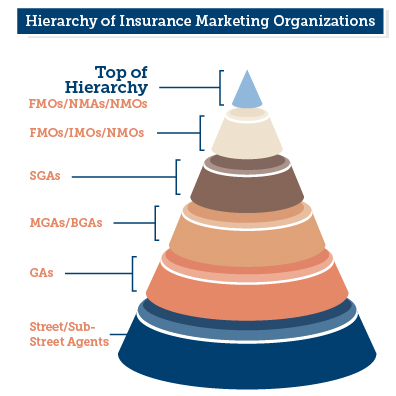

Role of Brokerage General Agencies in New York Life Distribution

Brokerage General Agencies (BGAs) play a pivotal role in New York Life’s extended distribution model by serving as strategic partners that recruit, train, and support independent insurance agents who sell New York Life products.

Drywall Business Insurance Ohio

Drywall Business Insurance OhioThese agencies do not employ agents directly but function as managing organizations that provide operational infrastructure, sales leadership, and back-end support—including licensing, compliance oversight, and performance tracking. By partnering with BGAs, New York Life maintains efficient access to a national network of producers without the overhead of direct employment, enabling faster market penetration and greater scalability.

BGAs often specialize in specific niches such as senior markets, high-net-worth clients, or business insurance, aligning with New York Life’s diverse product portfolio. The collaboration is mutually beneficial: BGAs gain access to a financially strong carrier with competitive products, while New York Life benefits from expanded agent representation and increased policy issuance through trusted intermediaries.

Function and Benefits of Independent Marketing Organizations (IMOs)

Independent Marketing Organizations (IMOs) are essential partners in New York Life’s external sales ecosystem, offering essential support services to independent agents marketing the company’s life insurance and annuity products.

An IMO typically provides training programs, sales tools, marketing materials, compliance guidance, and case management support, enabling agents to effectively position New York Life’s offerings to clients.

Evaluate The Insurance Company Insureon On Business Personal Property Insurance

Evaluate The Insurance Company Insureon On Business Personal Property InsuranceThese organizations often represent multiple carriers, but when they choose to affiliate with New York Life, it signifies confidence in the carrier’s financial stability, product competitiveness, and agent compensation structure. IMOs streamline the agent experience by aggregating technology platforms, simplifying appointment processes, and facilitating commission processing.

For New York Life, aligning with reputable IMOs means broader market visibility, increased production volume, and access to experienced sales professionals who can deliver personalized financial solutions to a wide demographic.

Regulatory and Operational Oversight in IMO and BGA Partnerships

New York Life maintains strict regulatory and operational oversight over its relationships with Brokerage General Agencies and Independent Marketing Organizations to ensure compliance, ethical sales practices, and policyholder protection. All IMOs and BGAs must undergo a formal appointment process and adhere to New York Life’s underwriting guidelines, suitability standards, and anti-fraud protocols.

The company conducts regular audits, monitors sales activity, and requires ongoing training to maintain high service and compliance standards across its distribution network. These partnerships are governed by contractual agreements that define responsibilities, compensation structures, and data privacy obligations, ensuring transparency and accountability.

Evaluate The Insurtech Company Hiscox On Small Business Insurance

Evaluate The Insurtech Company Hiscox On Small Business InsuranceFurthermore, New York Life leverages advanced technology platforms to track policy submissions, monitor producer activity, and deliver real-time support, reinforcing its commitment to operational integrity. This robust oversight mechanism helps safeguard the company’s reputation and ensures that all customers receive accurate, ethical, and professionally delivered financial advice.

| Aspect | Description | Key Benefit for New York Life |

|---|---|---|

| Brokerage General Agencies (BGAs) | Intermediaries that manage independent agents, offering leadership, compliance, and operational support in selling insurance products. | Expands national agent network and increases market reach without direct employment. |

| Independent Marketing Organizations (IMOs) | Organizations that provide training, marketing, technology, and administrative support to agents representing multiple carriers. | Enhances agent productivity and accelerates product distribution through streamlined support systems. |

| Compliance & Oversight | Regular audits, training mandates, and adherence to regulatory standards ensure ethical and legal sales practices. | Maintains New York Life’s reputation for integrity, financial strength, and policyholder protection. |

Detailed Guide to New York Life Insurance Company Brokerage General Agency IMO

Is New York Life Insurance Company affiliated with a brokerage general agency or IMO?

New York Life Insurance Company is not affiliated with a brokerage general agency (BGA) or an insurance marketing organization (IMO) in the traditional sense. Instead, it operates through a captive agency model, primarily utilizing its own in-house network of agents who are either employees or independent contractors affiliated directly with New York Life.

Unlike many other life insurance carriers that rely heavily on third-party BGAs or IMOs to distribute their products, New York Life maintains greater control over distribution by supporting its agents directly through proprietary tools, training, and administrative services.

This structure enables consistent brand representation and service standards. While some independent agents may offer New York Life products under specific arrangements, the company does not position itself as a carrier driven by external marketing organizations.

Understanding New York Life’s Distribution Model

- New York Life utilizes a hybrid agency system composed of both career agents and financial professionals, many of whom operate under the New York Life brand and are supported directly by the company’s regional offices.

- The company emphasizes long-term relationships with its representatives, providing centralized resources such as underwriting support, technology platforms, and professional development, minimizing reliance on external agencies.

- Although some agents may belong to independent networks or affiliations, New York Life does not contract through or delegate authority to brokerage general agencies or IMOs as part of its core business model.

Differences Between BGAs/IMOs and New York Life’s Approach

- Brokerage general agencies and IMOs typically represent multiple insurance carriers, train agents, and provide back-office support, whereas New York Life manages most of these functions internally.

- Many insurers partner with IMOs to expand market reach quickly, but New York Life has historically grown its distribution network organically, relying on direct recruitment and training.

- Agents representing companies tied to IMOs often have incentives tied to product sales volume across carriers, while New York Life agents typically focus on holistic financial planning using primarily New York Life products.

Independent Representation and Exceptions

- In certain cases, independent financial advisors or broker-dealers affiliated with third-party firms may offer New York Life insurance products if they have established selling agreements with the company.

- These arrangements, however, are exceptions and do not involve formal affiliation with a BGA or IMO as the primary distribution channel for New York Life.

- The company maintains strict standards for product presentation and agent qualifications, even in independent distribution scenarios, ensuring alignment with its corporate values and regulatory compliance.

Does New York Life Insurance Company provide brokerage services through its General Agency or IMO?

No, New York Life Insurance Company does not provide brokerage services through its General Agencies or through Independent Marketing Organizations (IMOs) in the way that some other financial services firms might.

Instead, New York Life operates primarily through a dedicated, exclusive network of agents who are either employees or independent contractors affiliated directly with the company. These agents are focused on selling New York Life’s own portfolio of insurance, annuities, and investment products rather than offering a range of third-party products through a brokerage platform.

While the company does have arrangements with certain third-party providers for specific products—such as long-term care insurance or certain investment options—these are typically made available through strategic partnerships rather than through a full-service brokerage model.

Additionally, New York Life maintains a distinction between its agent roles and broker-dealer functions, even though some agents may hold securities licenses (via broker-dealer affiliates like New York Life Distributors LLC) to sell investment products.

Therefore, although agents may offer a broad range of financial products, including securities, these offerings are structured within a product distribution framework rather than an open brokerage or advisory platform managed by General Agencies or IMOs.

Structure of New York Life's Distribution Network

- New York Life operates through a proprietary distribution model, relying on a force of career agents who are dedicated exclusively to selling New York Life products, ensuring alignment with the company's standards and long-term service goals.

- These agents may be salaried employees in the early stages of their careers or transition to independent contractor status, but they remain closely affiliated with New York Life and are not independent brokers free to sell competing insurers’ policies under their own brokerage.

- The company does not delegate product distribution authority to IMOs in the same way some insurers do; instead, agent recruitment and oversight are centralized or managed through regional managerial agencies under New York Life’s direction, reinforcing control over service quality and sales practices.

Role of New York Life Distributors LLC in Product Offerings

- New York Life Distributors LLC serves as the broker-dealer affiliate of New York Life, enabling agents who hold appropriate licenses to offer variable annuities, mutual funds, and other investment products regulated by the Securities and Exchange Commission (SEC) and FINRA.

- This structure allows agents to provide comprehensive financial planning solutions but within a controlled environment; the products available are approved and distributed through this regulated affiliate, not through open brokerage platforms managed by General Agencies or IMOs.

- Agents must register with New York Life Distributors LLC and comply with licensing, continuing education, and regulatory oversight requirements, ensuring that investment product sales are conducted under a supervised framework rather than as independent brokerage activities.

Differences Between Agency Models and Brokerage Services

- A General Agency in the New York Life system functions as an extension of the company, responsible for recruiting, training, and supporting agents—but it does not operate as a brokerage firm authorized to offer products from multiple insurers or financial institutions.

- Independent Marketing Organizations (IMOs) typically align with multiple insurance carriers and enable agents to compare and sell a wide range of third-party products, a model which contrasts with New York Life’s brand-exclusive approach.

- New York Life emphasizes product consistency, financial strength, and long-term client relationships, which aligns with its closed distribution model; it does not empower its agencies or partners to act as brokers offering competing life insurance or investment products from other companies.

Is New York Life Insurance Company currently operating as an active brokerage general agency or IMO?

No, New York Life Insurance Company is not currently operating as an active brokerage general agency or IMO (Independent Marketing Organization). It functions primarily as a mutual life insurance company that distributes its products through a proprietary network of career agents who are typically exclusive to New York Life. Unlike IMOs or brokerage general agencies, which operate independently and represent multiple insurance carriers, New York Life maintains a direct sales model focused on in-house distribution.

What Is the Distribution Model of New York Life Insurance Company?

- New York Life utilizes a career agent model, where sales professionals are directly appointed with the company and focus exclusively on New York Life products, ensuring brand consistency and deep product knowledge.

- The company does not rely on third-party brokers or external agencies to distribute its insurance and financial products, differentiating it from insurers that partner with IMOs or brokerages.

- This controlled distribution approach allows New York Life to maintain high service standards and direct oversight of client interactions, aligning with its long-term relationship-focused strategy.

How Does New York Life Differ From an IMO or Brokerage General Agency?

- IMOs and brokerage general agencies typically represent multiple insurance carriers and earn commissions by placing business with various companies, while New York Life agents work solely for one carrier—New York Life.

- Brokerage general agencies often provide back-end support, training, and marketing to independent agents across different brands, whereas New York Life offers internal support structures exclusively for its own agent force.

- New York Life does not operate as a third-party management entity for independent agents selling competing products, which is a key characteristic of an IMO or general agency.

Does New York Life Partner With Independent Agents or Brokers?

- While New York Life primarily relies on its exclusive agents, it may have limited affiliations with certain financial institutions or registered representatives for distributing specific products like annuities or long-term care insurance.

- These arrangements do not classify New York Life as a brokerage general agency or IMO, as the company does not act as a sponsor or managing entity for independent agent networks selling multiple carriers.

- Any external partnerships are supplementary and structured to complement the core agency model, not to shift the company toward a multi-carrier brokerage framework.

Is New York Life Insurance Company a captive brokerage general agency or independent IMO?

New York Life Insurance Company is not a captive brokerage general agency nor an independent IMO (Independent Marketing Organization). Instead, it operates as a mutual life insurance company with a primarily captive agency model.

This means that New York Life employs a force of career agents who are exclusive to the company and sell only New York Life products. These agents are typically paid via a salary and commission structure and are trained and supported directly by the company.

While the company does collaborate with certain external brokers and financial professionals, its core distribution method relies on its own dedicated sales force, which aligns more closely with a captive model than with independent distribution channels such as IMOs.

What Is a Captive Brokerage General Agency?

- A captive brokerage general agency refers to an organization that exclusively represents one insurance carrier or a select group of carriers, restricting its agents to selling only those brands’ products. These agencies often receive support, training, and marketing resources directly from the insurer.

- Captive agencies typically maintain a close operational relationship with the insurer, and agents may be considered employees or contractually bound representatives, which limits their ability to offer competitive products from other companies.

- This model ensures brand consistency and focused product knowledge but may limit consumer choice compared to independent models. New York Life’s career agent system closely mirrors this structure, although the company itself functions as the insurer rather than a third-party agency.

What Defines an Independent IMO?

- An Independent Marketing Organization (IMO) is a third-party entity that partners with multiple insurance carriers to recruit, train, and support independent agents who sell a variety of insurers’ products. IMOs do not underwrite policies but serve as distribution enablers.

- Agents affiliated with IMOs operate independently and are not employed by any single insurer, allowing them to offer clients products from competing companies to best meet diverse needs.

- IMOs generate revenue through overrides or commissions from the carriers they represent. Since New York Life does not function as a third-party distributor for multiple carriers, it does not meet the definition of an IMO, independent or otherwise.

How Does New York Life’s Distribution Model Work?

- New York Life maintains a proprietary sales force known as New York Life Agents, who are contracted exclusively to sell New York Life products. These agents are supported by regional offices and receive comprehensive training directly from the company.

- In addition to its career agency force, New York Life partners with independent broker-dealers, banks, and financial advisors through its New York Life Distributors arm. This allows broader market access while maintaining separation from the captive agent model.

- The company also offers products through worksite marketing and member-based organizations, but these arrangements are still governed by New York Life’s underwriting and compliance standards. This hybrid approach combines elements of captive distribution with selective independent partnerships, without aligning fully with the IMO structure.

Frequently Asked Questions

What is the New York Life Insurance Company Brokerage General Agency IMO?

The New York Life Insurance Company Brokerage General Agency IMO is an independent marketing organization affiliated with New York Life. It supports insurance producers by providing access to New York Life’s products, training, and resources. As an IMO, it operates independently while maintaining a strategic partnership to distribute life insurance, annuities, and other financial products. Agents benefit from New York Life’s strong reputation and financial strength.

How does the IMO structure benefit agents working with New York Life?

The IMO structure allows agents greater autonomy while gaining access to New York Life’s robust product portfolio and support systems. Agents receive training, marketing tools, and administrative assistance, helping them serve clients more effectively. Being part of an IMO offers flexibility in business management while still being backed by a financially stable and trusted insurance provider like New York Life.

Can independent agents join the New York Life Brokerage General Agency IMO?

Yes, independent agents can join the New York Life Brokerage General Agency IMO if they meet licensing and qualification requirements. The IMO recruits agents interested in offering New York Life’s insurance and financial products. Agents maintain independence in their operations while benefiting from the brand strength, product suite, and ongoing support provided through both New York Life and the IMO partnership.

What types of insurance products are offered through this IMO?

Through the New York Life Brokerage General Agency IMO, agents can offer a wide range of products including term and whole life insurance, universal life policies, annuities, long-term care insurance, and retirement solutions. These products are underwritten by New York Life, known for its financial strength and customer service. Agents use these offerings to help clients achieve protection and wealth planning goals.

Leave a Reply