Online Life Insurance Prices

Online life insurance prices have transformed the way consumers shop for coverage, offering transparency, convenience, and competitive rates at their fingertips.

With the rise of digital platforms and automated underwriting, individuals can now compare multiple policies in minutes, often securing lower premiums than through traditional channels. Factors such as age, health, lifestyle, and coverage amount directly influence pricing, but online tools allow for quick customization and real-time quotes.

Additionally, the elimination of face-to-face agent meetings reduces overhead costs, translating into savings for buyers. As demand for speed and simplicity grows, online life insurance continues to reshape the industry, making protection more accessible and affordable than ever before.

Drywall Business Insurance Ohio

Drywall Business Insurance OhioUnderstanding Online Life Insurance Prices: What You Need to Know

Shopping for life insurance online has become increasingly popular due to its convenience, transparency, and competitive pricing.

Online life insurance prices can vary significantly depending on multiple factors, including policy type, coverage amount, applicant age, health status, lifestyle habits, and even the insurance provider. By leveraging digital platforms, consumers can quickly compare quotes from multiple insurers, making it easier to find affordable and suitable coverage.

Unlike traditional methods that often require in-person meetings with agents, online systems use automated underwriting and instant quote tools to provide pricing information within minutes. This shift has not only reduced overhead costs for insurers but also resulted in more transparent and often lower premiums for consumers.

Furthermore, many online providers now offer tools such as calculators and comparison features, enabling users to fine-tune options and understand exactly what influences pricing. However, while online platforms offer simplicity, it’s essential to verify the credibility of insurers and understand policy details beyond just the price.

Evaluate The Insurance Company Insureon On Business Personal Property Insurance

Evaluate The Insurance Company Insureon On Business Personal Property InsuranceFactors That Influence Online Life Insurance Costs

Several key factors determine the price of life insurance when shopping online. First, age is one of the most significant variables—premiums typically increase with age due to higher mortality risk.

Health status, including medical history and current conditions such as diabetes or high blood pressure, heavily impacts pricing; many online insurers use quick health questionnaires to estimate risk and provide instant quotes.

Lifestyle choices, such as smoking or participation in high-risk activities, also elevate premiums. Policy type plays a critical role, with term life insurance generally being more affordable than whole or universal life policies.

The coverage amount (death benefit) directly affects cost—higher payouts mean higher premiums. Additionally, duration of coverage (e.g., 10, 20, or 30-year term) influences pricing, as does the applicant’s occupation and driving record. Online platforms often use real-time algorithms to adjust quotes based on these inputs, allowing for personalized pricing in seconds.

Evaluate The Insurtech Company Hiscox On Small Business Insurance

Evaluate The Insurtech Company Hiscox On Small Business InsuranceTerm Life vs. Whole Life: Comparing Online Prices

When comparing life insurance online, one of the most important decisions is choosing between term life and whole life insurance, each with distinct pricing structures. Term life insurance offers coverage for a set period (e.g., 10 to 30 years) and is typically the most affordable option, especially for young and healthy individuals.

Because it lacks a cash value component, term policies focus solely on the death benefit, resulting in lower online quotes. In contrast, whole life insurance provides lifelong coverage and includes a savings or cash value element that grows over time. This added benefit makes whole life significantly more expensive—often five to ten times the cost of a comparable term policy.

Online price comparisons often highlight this stark difference, helping consumers make informed choices based on their financial goals. While term life is ideal for temporary needs such as income replacement or mortgage protection, whole life appeals to those seeking permanent coverage and long-term wealth accumulation.

How Online Quotes and Instant Approval Affect Pricing

The rise of instant quotes and automated underwriting has transformed how online life insurance prices are determined and delivered. Traditional applications could take weeks for medical exams and manual reviews, delaying both approval and pricing clarity.

Finance And Insurance Business Relocation

Finance And Insurance Business RelocationToday, many insurers offer no-exam policies with online applications that use data from prescription records, credit reports, and DMV databases to assess risk instantly. This streamlined process reduces administrative costs, which can lead to lower premiums for consumers. Additionally, real-time quote engines allow users to compare offers from multiple insurers side by side, promoting competitive pricing.

However, it's important to note that while instant approvals are convenient, they may come with slightly higher rates than fully underwritten policies due to the limited medical data used. Nevertheless, for healthy applicants, simplified issue or guaranteed issue policies available online offer fast coverage at predictable prices, especially beneficial for those seeking urgent protection.

| Policy Type | Average Monthly Premium (Non-Smoker, 35-Year-Old) | Key Features | Best For |

|---|---|---|---|

| Term Life (20-year term, $500k) | $30–$45 | Limited duration, no cash value, affordable premiums | Temporary coverage, mortgage protection, income replacement |

| Whole Life ($250k) | $200–$350 | Lifelong coverage, builds cash value, fixed premiums | Estate planning, legacy building, long-term savings |

| Guaranteed Issue Life (No Medical Exam) | $50–$100 | Immediate coverage, limited death benefit, often no health questions | Seniors or those with pre-existing conditions |

Online Life Insurance Prices: A Comprehensive Guide to Rates and Coverage Options

What is the average monthly cost of a $1,000,000 life insurance policy online?

The average monthly cost of a $1,000,000 life insurance policy online varies significantly based on several key factors, including age, health, gender, lifestyle, and the type of policy selected. For a healthy 35-year-old non-smoker, a 20-year term life insurance policy with a $1,000,000 death benefit typically ranges from $40 to $60 per month.

A 45-year-old in similar health may pay between $80 and $120 monthly due to increased age-related risk. Permanent life insurance policies, such as whole life, are considerably more expensive, often costing several hundred dollars per month for the same coverage amount because they include a cash value component and offer lifelong coverage.

Financial Institutions Business Insurance

Financial Institutions Business InsuranceOnline rates are generally competitive due to digital underwriting and reduced overhead, but applicants must still undergo medical evaluations or answer detailed health questions to qualify for the best premiums.

Factors That Influence the Cost of a $1,000,000 Life Insurance Policy

- Age is one of the most significant determinants of life insurance cost. Premiums increase with age because the risk of mortality rises over time. A 30-year-old will pay substantially less than a 50-year-old for the same coverage, even with identical health profiles.

- Health status plays a crucial role in pricing. Insurers evaluate medical history, current conditions, prescription use, and results from medical exams. Individuals who are in excellent health, maintain a healthy weight, and have no chronic illnesses typically qualify for preferred rates.

- Lifestyle choices such as tobacco use, alcohol consumption, and participation in high-risk activities like skydiving or scuba diving can lead to higher premiums. Additionally, occupation and driving record are reviewed, as hazardous jobs or frequent traffic violations may increase perceived risk.

Term vs. Permanent Life Insurance: Cost Differences for $1M Coverage

- Term life insurance provides coverage for a specific period, such as 10, 20, or 30 years, and is the most affordable option for obtaining $1,000,000 in coverage. For example, a 20-year term policy for a healthy 40-year-old might cost between $50 and $90 per month.

- Whole life insurance, a type of permanent policy, offers lifelong protection and accumulates cash value over time. This added benefit results in much higher premiums—often ranging from $300 to over $600 monthly for the same $1,000,000 death benefit, depending on the insurer and applicant profile.

- Universal life insurance provides more flexibility than whole life, allowing adjustments to premiums and death benefits. However, it is still much more expensive than term insurance, with monthly costs typically starting in the hundreds of dollars for $1M coverage, making it less accessible for budget-conscious consumers.

How to Find Affordable $1,000,000 Life Insurance Online

- Compare multiple quotes from reputable insurers using online comparison tools. Websites from companies like Policygenius, LifeAnt, or Insurify allow users to view side-by-side quotes from various providers, helping identify the most competitive rates based on individual criteria.

- Improve your insurability before applying. Quitting smoking, losing weight, managing blood pressure and cholesterol, and limiting alcohol intake can help you qualify for lower premium tiers. Some insurers offer a preferred or super-preferred status for exceptionally healthy applicants, which can reduce costs by 20% or more.

- Consider the length and structure of the term. A 15-year term will usually have lower monthly payments than a 30-year term. Choosing a policy length that aligns with financial obligations—such as a mortgage or children's education—can balance coverage needs with affordability.

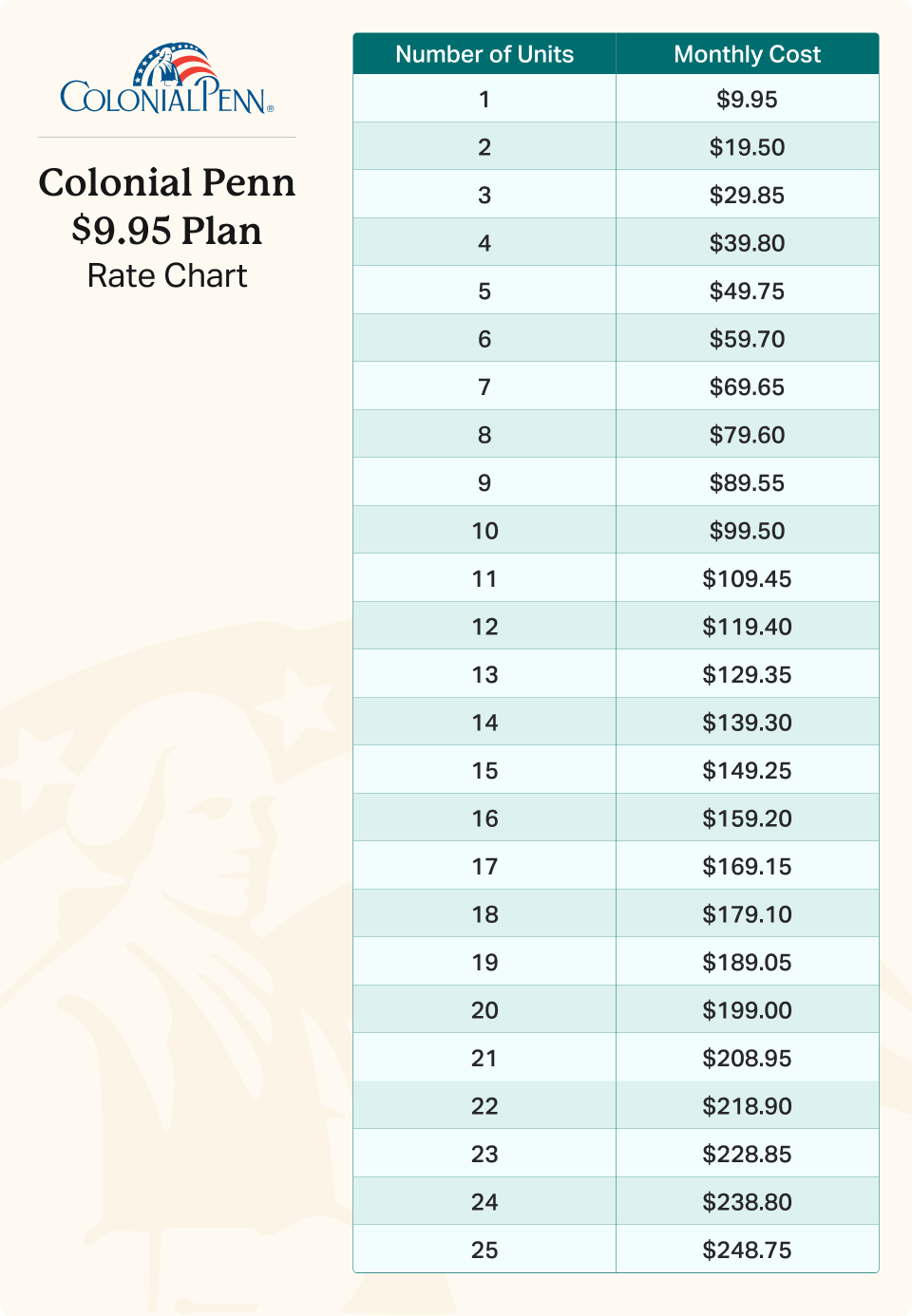

How much life insurance coverage can you get for $9.95 a month from Colonial Penn online?

What Coverage Amount Does Colonial Penn Offer for $9.95 per Month?

- Colonial Penn offers a simplified life insurance policy where $9.95 per month typically provides one unit of coverage, which is usually equivalent to $10,000 in life insurance benefits.

- The exact death benefit amount can vary based on factors such as age, health, and location, but the advertised rate generally corresponds with one unit priced at the $9.95 monthly rate.

- It's important to note that this rate is often available for a guaranteed acceptance policy with level premiums, meaning the price remains the same over time, but the coverage amount is relatively modest compared to traditional term life policies.

How Are Colonial Penn's Life Insurance Units Priced?

- Colonial Penn uses a unique unit-based pricing system where each unit of coverage comes with a fixed monthly cost; for many applicants, this is $9.95 per unit.

- The number of units a person can purchase depends on their age, gender, and health, with older or higher-risk applicants possibly approved for fewer units or required to pay a higher per-unit cost.

- Each unit generally provides $10,000 in death benefit, so two units would cost roughly $19.90 per month for $20,000 in coverage, allowing for scalable but predictable pricing.

What Factors Affect the Coverage You Receive for $9.95?

- Age is a significant factor—applicants under a certain age (often 65 or younger) are more likely to qualify for the advertised $9.95 rate per unit, while older individuals might face higher rates or reduced availability.

- Health status also plays a role; while Colonial Penn offers guaranteed acceptance for some plans, pre-existing conditions or high-risk health profiles can affect eligibility or premium costs.

- State regulations impact plan availability and pricing, meaning that the $9.95 rate for a $10,000 policy may not be accessible in all states due to differing insurance laws and underwriting standards.

What factors influence online life insurance prices?

Age and Health Condition

- One of the most significant factors affecting online life insurance prices is the applicant's age. Premiums generally increase with age because older individuals present a higher risk of mortality, leading insurers to charge more to offset potential claims.

- Health condition also plays a crucial role in determining pricing. Insurers evaluate medical history, current health status, and results from medical exams to assess life expectancy. Pre-existing conditions such as diabetes, heart disease, or cancer can lead to higher premiums or even denial of coverage.

- Additionally, lifestyle habits like smoking or excessive alcohol consumption are factored into the health assessment. Smokers typically pay significantly higher premiums due to increased health risks associated with tobacco use.

Policy Type and Coverage Amount

- The type of life insurance policy selected directly influences the price. Term life insurance, which provides coverage for a specific period, is generally more affordable than permanent life insurance, which includes a savings or investment component and lasts a lifetime.

- The amount of coverage, measured in the death benefit, also affects the cost. Higher coverage amounts require higher premiums because the insurer assumes greater financial risk in the event of a claim.

- Additional features such as riders for accidental death, critical illness, or waiver of premium can increase the overall cost. Each optional rider adds complexity and potential payout obligations for the insurer, reflected in the premium price.

Applicant's Occupation and Lifestyle

- Certain occupations are considered high-risk due to the nature of the work, such as construction, logging, or commercial fishing. Individuals in these fields may face higher premiums because of increased likelihood of injury or death.

- Lifestyle activities, including extreme sports like skydiving, scuba diving, or mountain climbing, are evaluated during underwriting. Engaging in such hobbies can lead to increased rates due to the associated risks.

- Insurers also consider the applicant’s driving record and criminal history. A history of DUIs or serious traffic violations may signal higher risk behavior, which can result in elevated insurance costs or coverage limitations.

Is $40 Monthly Expensive for Online Life Insurance Coverage?

- Age plays a significant role in determining life insurance costs. Younger individuals typically pay lower premiums because they pose a lower risk to insurers. For example, a healthy 30-year-old may easily find a policy for around $40 per month, while someone in their 50s might pay substantially more for the same coverage.

- Health status is another critical factor. Insurers evaluate medical history, current health conditions, lifestyle habits like smoking, and sometimes even driving records. A person with no major health issues and a clean medical profile is more likely to secure affordable rates, making a $40 monthly plan feasible.

- Lifestyle and occupation also impact pricing. High-risk activities or jobs—such as skydiving or commercial fishing—can increase premiums. Conversely, individuals with sedentary, low-risk lifestyles often qualify for the most competitive pricing available online.

Comparing $40 Policies Across Coverage Types

- For term life insurance, $40 per month can provide substantial coverage, especially for younger applicants. A 20- or 30-year term policy with a death benefit of $250,000 to $500,000 is often attainable at this price point through online insurers like Haven Life or Policygenius.

- Whole life insurance, which includes a cash value component, usually costs more. At $40 per month, coverage amounts may be significantly lower, sometimes limited to final expense or burial insurance policies with death benefits under $25,000.

- Online platforms frequently offer simplified or instant-issue policies that require no medical exam. While convenient, these may have higher rates or coverage limits. A $40 monthly budget may suffice for smaller no-exam policies but might fall short for larger, fully underwritten plans.

Is $40 Considered Affordable in Today’s Market?

- Market data from industry reports and insurance aggregators suggest that $40 per month is a competitive rate for a standard term life policy, particularly for individuals under 40 in good health. Many online insurers advertise rates starting as low as $20–$30 for 10–20 year terms with $250,000 coverage.

- However, affordability depends on individual needs. For someone seeking $1 million in coverage, $40 per month may be too low to secure adequate protection, especially with added riders or longer terms. In such cases, higher premiums would be necessary.

- Regional differences and inflation also affect pricing. While $40 might be affordable in areas with lower cost of living, it could represent a tighter budget constraint elsewhere. Online tools allow side-by-side comparisons to determine whether $40 aligns with average market rates for similar demographic profiles.

Frequently Asked Questions

What Factors Influence Online Life Insurance Prices?

Online life insurance prices are shaped by age, health, lifestyle, and coverage amount. Younger, healthier individuals typically pay less. Smoking, risky hobbies, and pre-existing conditions can increase premiums. The type of policy—term or permanent—also affects cost. Insurers use online applications to assess risk quickly, but quotes vary between providers. Comparing multiple online quotes helps find the best rate based on your personal profile and financial needs.

Are Online Life Insurance Quotes Accurate?

Yes, online life insurance quotes are generally accurate if you provide correct personal information. These quotes use real-time data from insurers and reflect current rates based on your age, health, and desired coverage. However, final approval may require a medical exam or underwriting, which could adjust the initial price. Always review the terms carefully and confirm whether the quoted price is guaranteed or an estimate.

Why Are Online Life Insurance Policies Often Cheaper?

Online life insurance policies often cost less due to reduced overhead for insurers. By selling directly through digital platforms, companies save on agent commissions and administrative expenses, passing those savings to customers. The streamlined application process also speeds up underwriting. Additionally, online tools allow easy comparison shopping, increasing competition and driving down prices. Consumers benefit from transparent pricing and more affordable coverage options.

Can I Buy Life Insurance Entirely Online?

Yes, many insurers allow you to buy life insurance entirely online. The process includes filling out an application, submitting health information, and sometimes completing a remote medical exam. Payments and policy documentation are handled digitally. Fully online policies, especially simplified issue or instant approval term life, offer convenience and speed. Ensure the provider is reputable, read all terms, and confirm that electronic signatures and delivery meet legal requirements for your area.

Leave a Reply