Porting Life Insurance

Porting life insurance refers to the ability to maintain coverage when transitioning between jobs or leaving group insurance plans.

This valuable option allows policyholders to retain their existing terms, coverage amount, and sometimes even premiums, without undergoing additional medical underwriting. As employment mobility increases and employer-sponsored benefits change, porting offers a critical safety net for individuals seeking continued financial protection.

It bridges gaps in coverage and ensures peace of mind during periods of professional transition. Understanding eligibility, timeframes, and policy terms is essential to fully benefit from porting life insurance.

Evaluate The Insurtech Company Hiscox On Small Business Insurance

Evaluate The Insurtech Company Hiscox On Small Business InsuranceUnderstanding Porting Life Insurance: What It Means and How It Works

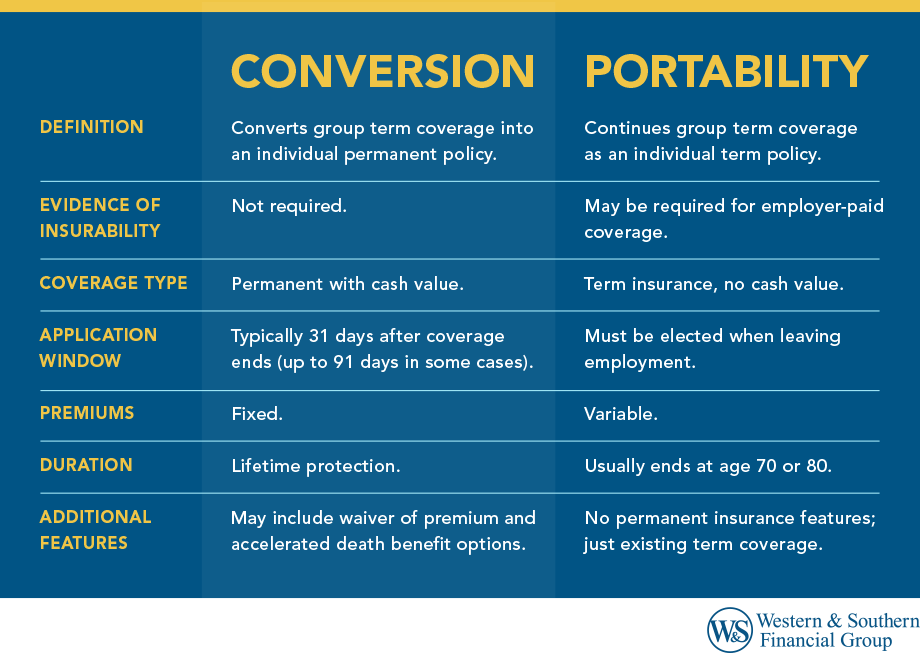

Porting life insurance refers to the process that allows individuals to transfer their existing life insurance coverage from one policy or provider to another without undergoing a new medical examination or facing significant coverage gaps.

This option is particularly relevant for those who are switching jobs, ending group life insurance through an employer, or seeking better terms in the individual market. While true portability is more commonly associated with group life insurance plans, certain policies may allow a form of conversion or continuation of coverage under specific conditions.

Understanding the rules surrounding porting life insurance is essential to maintain uninterrupted protection, especially during transitional life events such as retirement or changes in employment status. It ensures that individuals can preserve vital financial security for their loved ones without starting the underwriting process from scratch.

Eligibility Criteria for Porting Life Insurance Coverage

To qualify for porting life insurance, policyholders must typically meet certain eligibility requirements set by the insurer or employer-sponsored plan. These often include being an active participant in a group life insurance plan, maintaining coverage for a minimum duration, and initiating the porting process within a specified window—usually 30 to 60 days after employment ends or group coverage terminates.

Finance And Insurance Business Relocation

Finance And Insurance Business RelocationIn many cases, portability is only available for group term life insurance, allowing employees to convert their group coverage into an individual policy. However, the new individual policy may come with higher premiums due to age, health factors, or lack of group rates.

Insurers may also impose maximum coverage limits on the portable policy. Therefore, it's crucial for individuals to carefully review plan documents and consult with their HR department or insurance provider to confirm eligibility and understand all implications before making a decision.

Benefits and Limitations of Porting a Life Insurance Policy

Porting life insurance offers several key benefits, most notably the ability to retain coverage without proving insurability, which is especially valuable for individuals whose health has declined since initially obtaining the group policy.

It provides peace of mind during transitional periods and helps avoid potential lapses in protection that could leave dependents vulnerable. However, there are notable limitations to consider. Ported policies are typically more expensive than group rates since they lack the cost-sharing advantages of collective plans.

Financial Institutions Business Insurance

Financial Institutions Business InsuranceAdditionally, the coverage amount may be reduced, and the range of available policy types (e.g., term vs. permanent) may be limited. Some insurers only allow porting to specific kinds of term insurance, which may not align with an individual's long-term financial goals. As such, while porting ensures continuity, it's essential to weigh these trade-offs and explore alternative options in the individual market.

How to Initiate the Life Insurance Porting Process

Initiating the porting process begins with timely notification to the current insurer or plan administrator, usually shortly after a qualifying life event such as job loss or retirement.

The policyholder must formally request the portability option in writing or through an official application form provided by the insurance carrier. This application must be submitted within the stipulated timeframe to avoid losing the right to port.

Upon approval, the insurer will issue a new individual policy based on the original group coverage terms, though with adjusted premiums. It's crucial to review the new policy documents thoroughly to understand any changes in coverage, exclusions, or billing cycles. Keeping copies of all communications and confirming the effective date of the new policy ensures a smooth transition and continuous protection.

Frederick Business Insurance

Frederick Business Insurance| Aspect | Description | Key Considerations |

|---|---|---|

| Eligibility Window | Timeframe to apply for porting after leaving group coverage. | Usually 30–60 days; missing the deadline forfeits the right. |

| Medical Underwriting | Requirement for proving insurability. | Typically waived when porting, which is a major advantage. |

| Premium Costs | Price of the new individual policy. | Often higher than group rates due to individual risk pricing. |

| Coverage Amount | Level of death benefit transferred. | May be capped lower than original group coverage. |

| Policy Type Options | Available life insurance structures post-port. | Limited to term life in most porting scenarios. |

How to Port Life Insurance: A Step-by-Step Guide

What are the advantages of porting life insurance versus converting a policy?

Portability Maintains Existing Coverage Without Gaps

When an individual chooses to port their life insurance policy, they transfer the existing policy from one provider or plan to another while retaining the original terms and coverage. This process prevents any lapse in protection, which is crucial for individuals who rely on continuous coverage due to health conditions or financial obligations.

Unlike conversion, which may involve restructuring the policy, porting allows policyholders to keep their current death benefit, premium rates, and policy duration, assuming the new insurer accepts the transfer. This seamless transition ensures dependents remain protected throughout the process.

- Porting avoids potential waiting periods that may apply to new policies or conversions.

- It preserves accumulated cash value and riders, such as accidental death or waiver of premium.

- Continuity in coverage supports estate planning and creditor protection strategies without interruption.

One of the primary financial advantages of porting life insurance is the potential to maintain lower premium costs based on the original underwriting class. When a policy is converted—especially from a group to an individual plan—the insurer may reassess the applicant's current age, health, and risk profile, often leading to higher premiums.

Free Online Business Insurance Quote Quebec

Free Online Business Insurance Quote QuebecIn contrast, porting typically carries over the original premium structure, which was likely established when the individual was younger and healthier. This can result in significant long-term savings, especially for those with pre-existing conditions that might now make conversion expensive or unaffordable.

- Ported policies often lock in premiums calculated at an earlier age and improved health status.

- There is no need for new medical underwriting, reducing the risk of rate increases due to health changes.

- Insurers that allow porting usually apply consistent pricing, making budgeting more predictable over time.

Porting Offers Greater Flexibility and Control Over Policy Features

Choosing to port a life insurance policy generally provides the policyholder with enhanced control over their insurance structure. Portability allows individuals to retain specific policy provisions such as adjustable death benefits, flexible premium payments, or investment options in the case of permanent policies.

Converting a policy may limit these features or impose new restrictions based on the insurer’s conversion guidelines. Furthermore, porting supports customizations like changing beneficiaries, selecting different dividend options, or enhancing coverage through supplemental riders—all of which support long-term financial planning goals.

- Policyholders can preserve beneficial riders like long-term care or chronic illness benefits during the transfer.

- Porting supports modifications to payment schedules and policy ownership without starting from scratch.

- It enables transfer to insurers with stronger financial ratings or better customer service, enhancing policy management.

Can you transfer your life insurance policy to another provider?

![]()

Understanding Policy Portability and Transfer Options

- Life insurance policies are generally not transferred in the same way bank accounts or utility services might be, because each provider underwrites policies based on individual risk assessments. Instead of moving an existing policy, you typically need to apply for a new policy with a different insurer and then cancel or surrender your current one.

- Some permanent life insurance policies, such as whole or universal life, may allow you to transfer the cash value from one policy to another through a process known as a 1035 exchange. This IRS provision permits the tax-free transfer of funds between certain types of insurance contracts without incurring immediate tax liabilities.

- It’s critical to understand that starting a new policy means undergoing medical underwriting again, which could result in higher premiums if your health status has changed since your original policy was issued. Therefore, while direct transfer of a policy isn’t possible, strategic financial tools and new applications can achieve a similar outcome.

Steps to Switch Life Insurance Providers

- Begin by assessing your current policy, including coverage amount, premium payments, policy type, and any accumulated cash value. Review the terms and conditions to determine if there are any surrender charges or penalties for canceling early.

- Shop around with different insurance companies and request quotes based on your current age, health, and desired coverage. Compare not only premiums but also the financial strength of the insurers, customer service, and additional policy riders available.

- Once you've selected a new provider, complete the application process, which may include a new medical exam. Only after the new policy is approved should you formally cancel the old one to avoid any lapse in coverage that could leave beneficiaries unprotected.

When Transferring Makes Financial Sense

- Switching insurers may be beneficial if you can secure lower premiums for the same or better coverage, especially if your health has improved since your original policy was issued, or if market rates have decreased.

- Policyholders with permanent insurance might consider transferring cash value to a new policy offering better investment returns, lower fees, or more flexible withdrawal terms through a 1035 exchange.

- Another scenario where a switch makes sense is if your needs have changed—such as needing more coverage due to a new family member or mortgage—and your current provider cannot adequately meet those needs at a competitive rate.

Frequently Asked Questions

What does porting life insurance mean?

Porting life insurance refers to transferring your existing life insurance policy to a new insurer or keeping the same coverage when switching providers. It allows you to maintain your current terms, such as coverage amount and rates, without undergoing a new medical exam. Not all policies are portable, so it's essential to review your contract and consult your insurer to determine eligibility and process.

Can I port my life insurance policy to another company?

Yes, you may be able to port your life insurance policy, but it depends on your current insurer’s policies and the new provider’s acceptance criteria. Porting is more common with group life insurance, such as through an employer. Individual policies are typically not portable, so you may need to apply for a new policy. Always confirm with both insurers to understand your options and any limitations.

Do I need a new medical exam when porting life insurance?

In most cases, porting life insurance allows you to avoid a new medical exam, especially with group policies transferred during employment changes. However, if you're switching to an individual policy or a different type of coverage, a medical underwriting process may be required. Check with your new insurer to confirm their requirements and ensure continuous coverage during the transition.

What are the benefits of porting life insurance?

Porting life insurance helps maintain continuous coverage without new medical underwriting, preserving your current rates and benefits. It offers flexibility during major life changes like job loss or retirement. It can save time and avoid potential denial due to health changes. However, portability depends on policy type and insurer rules, so review your plan details to understand the full advantages and conditions.

Leave a Reply