Terms For Life Insurance

Life insurance is a crucial financial tool designed to provide security and peace of mind for individuals and their loved ones.

Understanding the key terms associated with life insurance is essential for making informed decisions. Policies typically involve beneficiaries, premiums, death benefits, and coverage duration, each playing a vital role in the overall function of the plan. Terms like term life, whole life, cash value, and underwriting affect how coverage works and who benefits.

Familiarity with these concepts helps individuals choose the right policy based on their needs, financial goals, and family circumstances. Knowledge empowers better planning for the future.

Geico Auto Business Insurance

Geico Auto Business InsuranceUnderstanding Key Terms for Life Insurance

Life insurance can be a crucial financial tool, providing security and peace of mind for you and your loved ones.

However, navigating the terminology associated with life insurance policies can be overwhelming, especially for first-time buyers. Understanding key terms such as premium, death benefit, and policyholder is essential to making informed decisions. Each term plays a significant role in defining the scope, cost, and benefits of a life insurance plan.

Familiarity with these concepts enables policyholders to compare different plans effectively, avoid misunderstandings, and choose coverage that aligns with their financial goals and personal circumstances. Knowledge of these terms also helps in communicating better with insurance agents and in reviewing policy documents more thoroughly.

A premium is the amount of money a policyholder pays to an insurance company to maintain life insurance coverage.

General Liability Business Insurance San Francisco CA

General Liability Business Insurance San Francisco CAPremiums can be paid on a monthly, quarterly, or annual basis, depending on the policy terms, and the cost is influenced by various factors such as age, health, lifestyle, occupation, and the amount of coverage desired. Failure to pay the premium within the grace period typically results in the policy lapsing, which means coverage ends.

Some policies offer level premiums, which remain the same throughout the term, while others may have increasing premiums based on age or other variables. Choosing the right premium payment structure is vital to ensuring long-term affordability and uninterrupted protection.

Understanding the Death Benefit

The death benefit is the amount of money paid by the insurer to the named beneficiaries upon the death of the insured person, assuming the policy is active.

This is the core purpose of life insurance and is typically tax-free to the recipient. The death benefit amount is determined when the policy is purchased and can be used by beneficiaries for various needs such as covering funeral expenses, paying off debts, replacing lost income, or funding education.

General Liability Insurance Cost Pressure Washing Business Florida Cost

General Liability Insurance Cost Pressure Washing Business Florida CostPolicyholders can often choose between a fixed death benefit or one that varies based on the policy type—such as term or permanent life insurance. Accurately assessing how much death benefit is needed ensures that dependents are adequately protected financially.

Defining the Policyholder and Beneficiary Roles

The policyholder is the individual who owns the life insurance policy, responsible for paying premiums and making decisions about coverage, such as selecting or changing the beneficiaries.

The beneficiary is the person or entity designated by the policyholder to receive the death benefit when the insured passes away. Beneficiaries can be primary—first in line to receive the benefit—or contingent, who receive the proceeds if the primary beneficiary is unable or unwilling to claim.

It's important to clearly define these roles and keep beneficiary designations up to date after major life events such as marriages, divorces, or the birth of children. Clear designation helps avoid legal complications and ensures the intended recipients receive the benefit efficiently.

General Liability Insurance For Texas Businesses

General Liability Insurance For Texas Businesses| Term | Definition | Importance |

|---|---|---|

| Premium | The periodic payment made to keep the life insurance policy active. | Determines affordability and sustainability of coverage over time. |

| Death Benefit | The payout received by beneficiaries upon the insured’s death. | Provides financial protection and support to loved ones. |

| Policyholder | The person who owns and manages the insurance policy. | Has control over policy decisions, including beneficiary selection. |

| Beneficiary | The individual or entity entitled to receive the death benefit. | Ensures the financial intent of the policy is fulfilled after death. |

| Term Life Insurance | Coverage that lasts for a specific period, such as 10, 20, or 30 years. | Offers affordable, temporary protection for key financial obligations. |

Understanding Life Insurance Terms: A Comprehensive Guide

What is the average cost of a $1,000,000 term life insurance policy based on common policy terms?

Factors Influencing the Cost of a $1,000,000 Term Life Insurance Policy

- Age is one of the most significant determinants of premium costs. Younger applicants, such as those in their 30s, typically pay substantially lower monthly or annual premiums compared to individuals in their 50s or 60s, as insurers view younger people as lower risk for early death.

- Gender also plays a role, with women generally receiving lower rates than men due to their longer average life expectancy. This statistical difference leads to slightly reduced premiums for female policyholders on a $1,000,000 term life policy.

- Lifestyle factors, including smoking, alcohol consumption, and participation in high-risk activities (like skydiving or scuba diving), can dramatically increase premiums. Applicants who smoke, for example, may pay two to three times more than non-smokers for the same coverage amount.

- For a 30-year-old non-smoking male purchasing a 20-year term policy with $1,000,000 in coverage, average annual premiums typically range from $400 to $600. The same policy for a female might cost between $300 and $500 annually due to actuarial life expectancy differences.

- A 40-year-old non-smoker might expect to pay between $600 and $900 per year for a 20-year term, with rates increasing further for a 30-year term policy—averaging $800 to $1,200 annually, depending on health classification.

- Applicants in their 50s face higher premiums due to increased risk; a 55-year-old in good health might pay $2,000 to $3,500 per year for a 20-year $1,000,000 term policy, especially if they have minor health concerns such as controlled high blood pressure or high cholesterol.

- Insurance companies assign health classifications—such as Preferred Plus, Preferred, Standard, or Substandard—based on medical exams, lab results, and lifestyle disclosures. A Preferred Plus applicant, representing excellent health, will receive the lowest available rates for a $1,000,000 policy.

- For example, a 35-year-old male in the Preferred Plus category might pay around $450 annually for a 25-year term, while the same individual classified as Standard could pay upwards of $750, showing how classifications directly affect cost.

- Pre-existing conditions such as diabetes, heart disease, or obesity can lead to a Substandard classification, resulting in significantly higher premiums or even denial of coverage. In such cases, insurers may offer policies with rated premiums (increased rates) to account for the elevated risk.

What are the four main types of life insurance policies based on policy terms?

Term Life Insurance

Term life insurance is a straightforward form of coverage that provides protection for a specified period, often ranging from 10 to 30 years. It is designed to offer a death benefit to beneficiaries if the policyholder passes away during the term.

This type of policy is generally more affordable than permanent options since it does not accumulate cash value. Term life insurance is ideal for individuals seeking temporary coverage to protect dependents during financially critical years, such as when raising children or paying off a mortgage.

- Provides coverage for a fixed period, such as 10, 15, 20, or 30 years

- Generally has lower premiums compared to permanent life insurance

- Does not build cash value; expires at the end of the term unless renewed

Whole Life Insurance

Whole life insurance is a type of permanent life insurance that offers lifelong coverage as long as premiums are paid.

In addition to providing a guaranteed death benefit, it includes a savings component known as cash value, which grows at a guaranteed rate over time. Policyholders can borrow against the accumulated cash value or withdraw funds under certain conditions. Whole life insurance is typically more expensive than term life due to its lifetime coverage and cash accumulation features.

- Provides lifelong coverage with fixed premiums that do not increase over time

- Includes a cash value component that grows at a guaranteed interest rate

- Offers policy loans and withdrawals, though they may affect the death benefit

Universal Life Insurance

Universal life insurance is a flexible form of permanent life insurance that allows policyholders to adjust their premiums and death benefits within certain limits.

Like whole life, it includes a cash value component, but the growth of this value is typically tied to current interest rates. This policy offers more control than whole life, enabling adjustments based on financial needs. However, its complexity and dependence on interest rates mean that careful management is required to maintain coverage.

- Allows adjustable premiums and death benefits to suit changing financial needs

- Cash value grows based on current interest rates, offering potential for higher returns

- Requires active management to ensure the policy remains in force

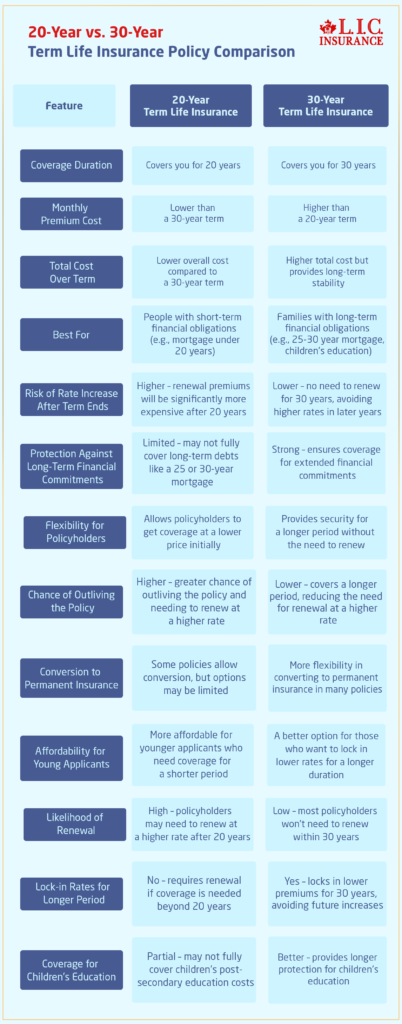

Should I choose a 20-year or 30-year term for my life insurance policy?

Understanding the Length of Financial Obligations

- Assessing how long your financial dependents will need coverage is essential when deciding between a 20-year and 30-year term life insurance policy. A 20-year term is often suitable for individuals with specific, time-bound responsibilities such as a mortgage with two decades remaining or children expected to be financially independent by that time.

- If you have long-term financial commitments like a 30-year mortgage, younger children, or a special needs dependent, a 30-year term might better align with the duration of these obligations. This ensures that protection extends far enough into the future to cover any potential gaps in financial security.

- Additionally, current income stability and retirement plans should factor into your decision. Someone planning to retire in 20 years may find a 20-year term sufficient, whereas someone expecting to work longer or continue providing for dependents past age 65 may benefit more from a longer 30-year policy.

- Premiums for a 30-year term are typically higher than those for a 20-year term because the insurance company assumes a greater risk by providing coverage over a longer period. The incremental cost must be weighed against your long-term budget and other financial priorities.

- Opting for a 20-year term often results in lower annual or monthly payments, which can free up funds for other investments, savings, or debt reduction. This affordability can be a deciding factor for those with tighter budgets but still require substantial protection during key life stages.

- However, locking in a 30-year term now may be more cost-effective in the long run than renewing or reapplying for coverage after a 20-year term expires, especially if your health declines. Premiums for new policies later in life can be significantly higher, making the initially higher 30-year premium a prudent investment.

Planning for Future Insurance Needs and Flexibility

- One key consideration is whether you will still need life insurance beyond 20 years. If your policy expires and you still have dependents or debts, requalifying for a new policy may be difficult or expensive, particularly if health issues arise. A 30-year term provides continuity without the need to reassess eligibility later.

- Some term policies offer conversion options, allowing you to convert a portion or all of the term coverage into permanent life insurance without a medical exam. This flexibility can be valuable, but it's often time-limited and may not fully compensate for the lapse in coverage after a 20-year term ends.

- Life circumstances can change unexpectedly—such as having more children, starting a business, or taking on new debt. A 30-year term offers a longer safety net that can accommodate unforeseen developments, while a 20-year term may require reevaluation and readjustment down the line, which could come with complications or higher costs.

Frequently Asked Questions

What Are the Common Terms Used in Life Insurance Policies?

Common terms in life insurance include premium, death benefit, beneficiary, term length, and underwriting. The premium is the amount paid for coverage, while the death benefit is the payout received by beneficiaries upon the insured’s death. The beneficiary is the person who receives the benefit. Term length refers to the policy’s duration, and underwriting is the risk assessment process used by insurers to determine eligibility and pricing.

What Does ‘Term Life Insurance’ Mean?

Term life insurance provides coverage for a specific period, such as 10, 20, or 30 years. If the insured dies during this term, the death benefit is paid to the beneficiary. It does not build cash value and expires at the end of the term if not renewed. Term life is often more affordable than permanent insurance and is ideal for temporary financial responsibilities like mortgages or children’s education.

What Is the Difference Between Term and Whole Life Insurance?

Term life insurance covers a set period and pays a death benefit if the insured dies within that term. It does not accumulate cash value. Whole life insurance provides lifelong coverage and includes a savings component that builds cash value over time. Whole life premiums are higher but offer permanent protection and potential investment growth, making it suitable for long-term financial planning and estate needs.

What Happens if I Outlive My Term Life Insurance Policy?

If you outlive your term life insurance policy, the coverage simply ends, and no death benefit is paid. You may have the option to renew the policy, often at a higher premium due to increased age. Some policies allow conversion to a permanent life policy without a new medical exam. Otherwise, you can apply for a new term policy if you still require coverage.

Leave a Reply