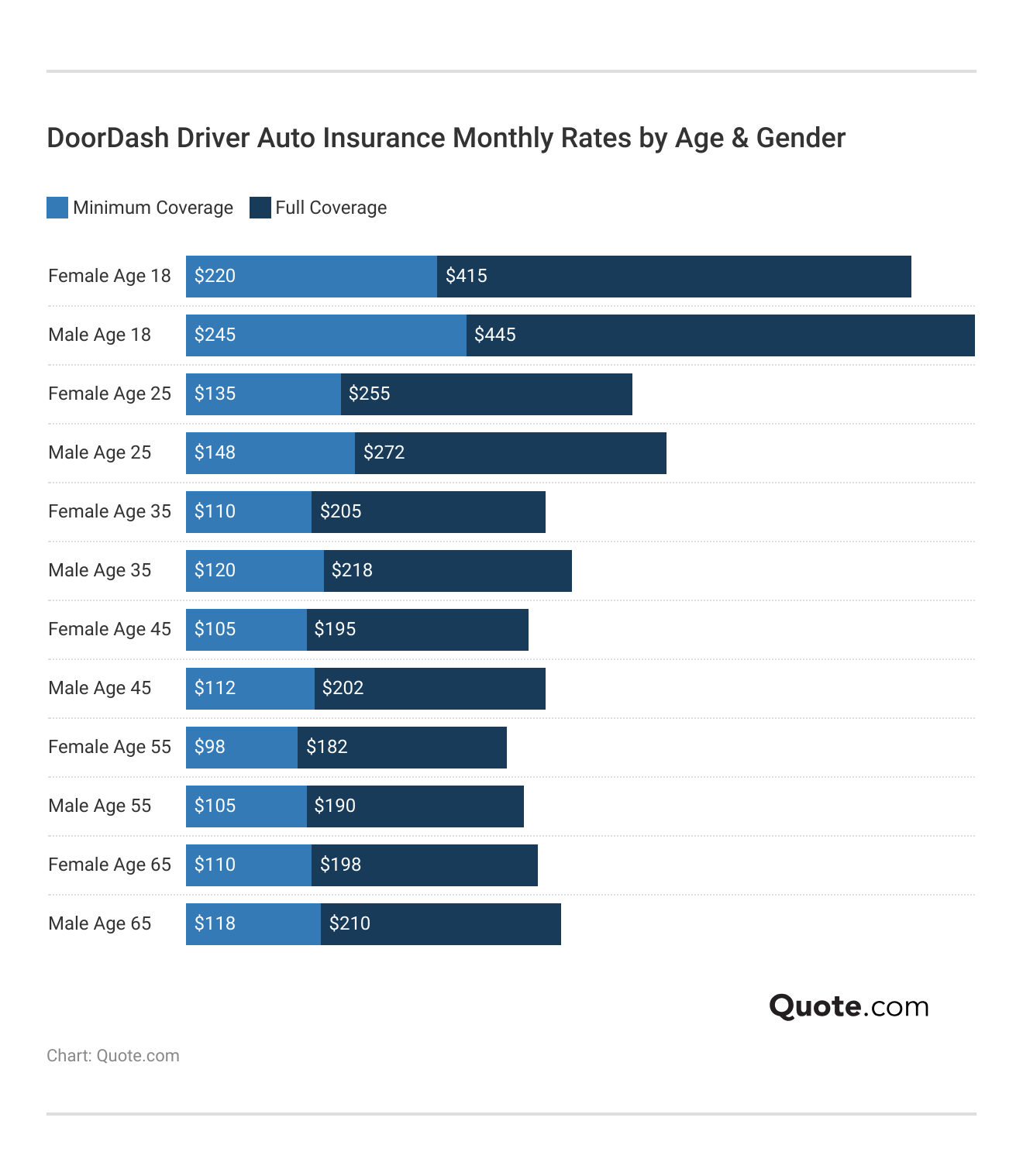

Do I Need Special Car Insurance For Doordash

Driving for Doordash offers flexibility and earning potential, but it also raises important questions about insurance coverage.

Personal car insurance policies typically don’t cover accidents that occur while making deliveries for food delivery platforms. This gap in coverage can leave drivers financially vulnerable. As a Doordash delivery driver, your vehicle transitions from personal to commercial use during delivery trips, which affects liability in the event of an accident.

Understanding Doordash’s insurance policy and whether supplemental coverage is necessary is essential. This article explores the risks, coverage options, and steps drivers should take to ensure they’re properly protected on the road.

Do You Have To Have Special Insurance For Doordash

Do You Have To Have Special Insurance For DoordashDo I Need Special Car Insurance For Doordash?

When driving for Doordash, one of the most important considerations is whether your current car insurance policy adequately covers you during food delivery activities. Most personal auto insurance policies explicitly exclude coverage for commercial use of your vehicle, and driving for a delivery service like Doordash is considered commercial activity.

This means that if you're involved in an accident while delivering orders and your insurer determines you were working at the time, your claim could be denied. While Doordash provides its own insurance coverage during specific periods of your delivery cycle—known as dash periods—this coverage only kicks in after you've accepted an order and are actively en route to pick up or deliver food.

Between logging into the app and accepting an order, there's a coverage gap, and this is where personal policies may fall short. Therefore, while you're not required to carry a special commercial insurance policy to deliver for Doordash, you may want to consider additional protection such as a rideshare endorsement or commercial policy for complete peace of mind.

When Does Doordash’s Insurance Coverage Apply?

Doordash offers intermittent liability insurance that activates only during certain phases of your delivery activity, known as Periods 2 and 3. Period 1—when you're logged into the app but haven't accepted a delivery—typically has minimal or no coverage from Doordash, so your personal auto insurance would need to fill the gap.

Do You Have To Have Special Insurance To Deliver Food

Do You Have To Have Special Insurance To Deliver FoodHowever, many personal insurers may not cover accidents that occur during this time if they determine you are engaged in commercial driving. Once you accept a delivery, Period 2 begins (driving to the restaurant), and Doordash provides liability coverage, usually including bodily injury and property damage to others. Period 3 covers you from the time you pick up the order until you complete the delivery.

During these active periods, Doordash provides primary liability insurance, but it doesn't cover damage to your own vehicle unless you carry comprehensive and collision coverage through your own insurer. Understanding these coverage periods is crucial for knowing when you’re protected and when you might be at risk.

A rideshare endorsement is an optional addition to your personal auto insurance policy that extends coverage to include periods when you’re using your vehicle for gig economy work, such as driving for Uber, Lyft, or delivering for Doordash.

While not required by Doordash, this endorsement can bridge the coverage gap during Period 1, when you’re logged into the app but haven't accepted a delivery. Without this endorsement, your personal insurer might deny a claim because they consider delivery work a commercial use of your car. Major insurers like GEICO, State Farm, and Allstate offer rideshare endorsements, usually for a small additional premium.

Does Condo Insurance Cover Special Assessments

Does Condo Insurance Cover Special AssessmentsThis endorsement ensures that your insurer won’t drop you or deny a claim simply because you're using your vehicle for food delivery. For drivers who deliver regularly, this added protection offers valuable security, especially considering the potential financial risk of a denied claim after an accident.

Commercial vs. Personal Auto Insurance: What’s the Difference?

The key difference between commercial and personal auto insurance lies in how the vehicle is used. Personal auto policies are designed for everyday commuting and personal errands, not for business-related driving.

When you make frequent trips, carry goods (like food), and use your vehicle to earn income—such as with Doordash—you’re engaging in commercial activity. Standard personal policies can exclude coverage in these cases, leaving you financially exposed. Commercial auto insurance, on the other hand, is built for business use and provides broader liability and vehicle damage protection. However, it's also significantly more expensive than personal insurance.

For Doordash drivers, a full commercial policy might be overkill unless you're delivering full-time or using a commercial vehicle. A more cost-effective option is a personal policy with a rideshare endorsement, which provides enhanced protection without the high cost of a full commercial plan, making it a smart middle ground for most gig drivers.

Does Special Event Insurance Cover Weather

Does Special Event Insurance Cover Weather| Insurance Scenario | Coverage Status | Key Notes |

|---|---|---|

| Personal Insurance Only | Limited/Excluded | May not cover commercial use; risk of claim denial during delivery |

| Doordash Insurance (Period 1) | No Coverage | When logged in but no delivery accepted—highest risk period |

| Doordash Insurance (Periods 2 & 3) | Liability Covered | Primary liability insurance provided; does not cover damage to your vehicle |

| Rideshare Endorsement | Enhanced Coverage | Covers gap in Period 1; recommended for regular drivers |

| Commercial Auto Policy | Full Coverage | Most comprehensive but costly; best for full-time delivery drivers |

Do You Need Special Car Insurance for DoorDash Deliveries?

What car insurance coverage is required for DoorDash delivery drivers?

Personal Auto Insurance Limitations for Delivery Drivers

Personal auto insurance policies are typically designed for personal use and do not provide coverage when the vehicle is being used for commercial purposes such as food delivery. Most standard policies explicitly exclude coverage if the driver is engaged in for-hire transportation or delivery services.

This means that if an accident occurs while actively delivering a DoorDash order, the driver’s personal insurance may deny the claim, leaving the driver financially liable for damages, medical expenses, or vehicle repairs. It’s essential for drivers to understand these limitations before beginning delivery work.

- Personal auto policies generally exclude commercial use, such as delivering food for pay.

- Using a personal vehicle for DoorDash without proper coverage can result in claim denials.

- Drivers risk significant out-of-pocket costs if found at fault in an accident during delivery.

DoorDash’s Provided Insurance Coverage During Deliveries

DoorDash offers insurance coverage to its delivery drivers, but the level of protection depends on the phase of the delivery. When a driver accepts an order and is en route to the restaurant or delivering to the customer (referred to as Periods 2 and 3), DoorDash provides contingent liability insurance.

How Much Is Special Event Liability Insurance

How Much Is Special Event Liability InsuranceThis coverage kicks in only after personal insurance has been exhausted and includes bodily injury and property damage liability. The coverage typically includes up to $1 million in liability protection. However, it does not cover damage to the driver’s own vehicle unless they purchase optional vehicle damage protection offered in certain states.

- DoorDash provides contingent liability insurance during active delivery phases (accepted order to drop-off).

- Coverage includes up to $1 million in liability for third-party injuries or property damage.

- The driver’s personal insurance is primary; DoorDash’s coverage applies only after personal insurance has been used.

Commercial Insurance and Gap Protection Options

To fully protect themselves, many DoorDash drivers opt for a commercial auto insurance policy or a rideshare endorsement added to their personal policy.

These specialized policies bridge the gap between personal coverage and DoorDash’s insurance. Some insurance companies now offer rideshare-specific policies that provide continuous coverage during all phases of delivery, including periods when the app is on but no order has been accepted.

In addition, DoorDash offers optional vehicle damage protection in select regions, which covers repairs to the driver’s car after a covered incident, reducing financial risk. Drivers should compare available options based on their state regulations and driving frequency.

- Rideshare or commercial endorsements extend personal coverage to include delivery-related driving.

- Available options vary by state and insurer, so drivers must research local availability.

- Optional vehicle damage protection from DoorDash helps cover repair costs when the driver’s car is damaged during a delivery.

What Is the Most Cost-Effective Car Insurance Option for Doordash Drivers?

- Many Doordash drivers start with their existing personal auto insurance policies, which may offer limited coverage during delivery periods, particularly when the app is active. However, standard personal insurance policies typically do not cover commercial use of a vehicle, which includes food delivery services.

- Some insurers, such as State Farm, Geico, and Allstate, offer rideshare endorsements or specialized add-ons that extend coverage during Period 1 (when the app is on but no delivery is accepted) and Period 2 (when en route to pick up food). These endorsements can bridge the gap between personal and commercial insurance at a relatively low additional cost.

- For Doordash drivers who only log a few hours weekly, adding a rideshare endorsement to a personal policy often represents one of the most cost-effective solutions, as it avoids the higher premiums associated with full commercial policies while providing essential protection during active delivery periods.

Commercial Auto Insurance for Full-Time Dashers

- Drivers who work for Doordash full time or spend many hours behind the wheel may need commercial auto insurance, which is designed for vehicles used for business purposes. This type of policy offers comprehensive coverage throughout all phases of food delivery, including driving to pick up orders and transporting food to customers.

- While commercial insurance premiums are generally higher than personal policies, they provide greater liability and collision protection that personal policies often exclude during commercial use. This reduces the risk of out-of-pocket expenses in the event of an accident while delivering.

- For drivers whose vehicles are primarily used for delivery, investing in a commercial policy can be cost-effective in the long run, as it prevents potential claim denials and policy cancellations that might occur if a personal insurer discovers frequent commercial use.

Hybrid Policies and Usage-Based Insurance Options

- A growing number of insurers now offer hybrid policies that blend elements of personal and commercial coverage, tailored specifically for gig economy drivers. Companies like Jerry, Metromile (now part of Root), and Mercari Insurance provide pay-per-mile or usage-based policies that charge premiums based on actual miles driven for delivery.

- These models can be highly cost-effective for part-time or low-mileage Doordash drivers who want proper coverage without paying for full-time commercial insurance. For example, a driver who delivers only on weekends will pay significantly less than one driving 40 hours per week.

- Usage-based policies often include features like mobile tracking, which verifies when the Doordash app is active, and automatically adjusts coverage levels. This flexibility ensures drivers are protected during delivery periods while minimizing costs during personal use, making them a smart financial choice for many gig workers.

Does being a DoorDash driver increase your car insurance rates?

Does Commercial Use Affect Personal Car Insurance?

When you drive for DoorDash, your vehicle is being used for commercial purposes, which differs significantly from standard personal use like commuting or running errands. Most personal auto insurance policies explicitly exclude coverage for commercial activities.

As a result, if you're involved in an accident while delivering for DoorDash and haven't informed your insurer, they may deny your claim or even cancel your policy. Insurers assess risk based on how a vehicle is used, and delivery driving increases exposure to risk due to higher mileage and time spent on the road. This change in usage pattern can lead insurers to reclassify your policy or raise your premiums upon discovery.

- Standard personal insurance policies typically do not cover accidents that occur during delivery activities unless you have specific gig economy coverage.

- Insurance companies may discover commercial use through accident claims, where detailed driving logs or app usage data can expose delivery activity.

- Driving for DoorDash increases the likelihood of claims, which may trigger a policy review or adjustment in rates when reported.

Does DoorDash Provide Any Insurance Coverage?

DoorDash does offer some level of insurance coverage while you’re actively working, but it's important to understand the limitations. Their insurance is provided in three periods: when you’re en route to pick up an order, when you have an order in your possession, and while delivering it.

However, when the app is on but you haven’t accepted a delivery (Period 0), you are not covered by DoorDash’s commercial insurance. During this period, your personal insurance would be responsible, and if it doesn't cover commercial use, you could be financially exposed. This gap creates a risky scenario where neither DoorDash nor your insurer may cover damages.

- DoorDash's insurance activates only after you accept a delivery, leaving a coverage gap when the app is on but no delivery is active.

- The coverage includes liability, uninsured motorist protection, and collision/comprehensive during active delivery periods, subject to deductibles.

- Drivers must still maintain a valid personal auto policy, as DoorDash insurance is supplemental and doesn't replace personal coverage.

Should You Inform Your Insurance Company About Driving for DoorDash?

Yes, you should inform your insurance provider if you plan to or are already driving for DoorDash. Failing to disclose this information is considered material misrepresentation and can lead to serious consequences.

Some insurers offer ride-share or delivery endorsements that extend coverage to gig economy activities. These endorsements often come with higher premiums, but they provide necessary protection during all periods of app usage. By being transparent, you ensure that you're properly covered and avoid denial of claims, which could result in significant out-of-pocket expenses.

- Contacting your insurer allows you to add a commercial use or gig economy endorsement, which adjusts your policy to reflect actual driving habits.

- While premiums may increase, the added protection is essential for avoiding financial liability in case of an accident during deliveries.

- Some insurers specialize in policies for gig workers, offering more accurate pricing based on delivery driving risks and usage patterns.

Frequently Asked Questions

Do I Need Special Car Insurance For Doordash?

Yes, you need additional insurance when delivering for Doordash. Your personal car insurance may not cover accidents that happen while you're delivering.

Doordash provides some commercial coverage, but it only activates during specific delivery periods. It's wise to inform your insurer about your delivery work and consider a rideshare endorsement or commercial policy for full protection during all stages of delivery.

Does Doordash Provide Insurance Coverage?

Yes, Doordash offers limited commercial insurance coverage. It applies only after you've accepted a delivery (Period 2) and while you're en route to drop off the order (Period 3).

The coverage includes liability, uninsured motorists, and damage to your vehicle. However, it doesn't cover accidents during Period 1 (when you're logged in but haven't accepted a dash). Personal insurance gaps make supplemental coverage important.

Will My Personal Car Insurance Cover Me While Doordashing?

Most personal car insurance policies exclude coverage for commercial activities like food delivery. If you're in an accident while Doordashing, your insurer may deny the claim if they find you were working.

To avoid this risk, inform your insurance provider about your delivery work. Some insurers offer rideshare add-ons that extend protection during all delivery periods, making them a smart investment.

What Insurance Gaps Exist When Delivering for Doordash?

The main insurance gap occurs in Period 1—when you're logged into the app but haven't accepted a delivery. During this time, neither your personal insurance nor Doordash's coverage fully applies.

Accidents that occur here could leave you financially responsible. To close this gap, consider a rideshare insurance policy, which bridges coverage between personal and commercial use, ensuring continuous protection throughout your delivery shifts.

Leave a Reply