Do I Need Special Insurance For Uber

Riding for Uber can be a flexible and rewarding way to earn income, but it also raises important questions about insurance coverage. Standard personal auto insurance policies are typically not designed to cover commercial driving activities, leaving drivers vulnerable during trips.

Uber does provide its own insurance, but the coverage varies depending on the phase of the ride—waiting for a request, en route to pick up a passenger, or during a trip. Understanding these distinctions is crucial, as gaps in coverage could result in out-of-pocket expenses after an accident. Many drivers opt for additional insurance to ensure comprehensive protection throughout all stages of driving for Uber.

Do I Need Special Insurance For Uber?

Yes, when driving for Uber, you do need to understand the insurance requirements because your standard personal auto insurance may not cover you during all phases of your rideshare activity.

Do You Have To Have Special Insurance For Doordash

Do You Have To Have Special Insurance For DoordashUber provides its own insurance coverage, but it only applies during specific periods of your trip cycle—such as when you have a ride request, are en route to pick up a passenger, or are transporting a passenger. When the app is off, you're only covered by your personal auto insurance.

However, if you're caught using your vehicle for ridesharing without informing your insurer or without proper rideshare coverage, your claim could be denied. Therefore, many drivers opt for a rideshare endorsement or a commercial policy to ensure continuous protection throughout the entire process.

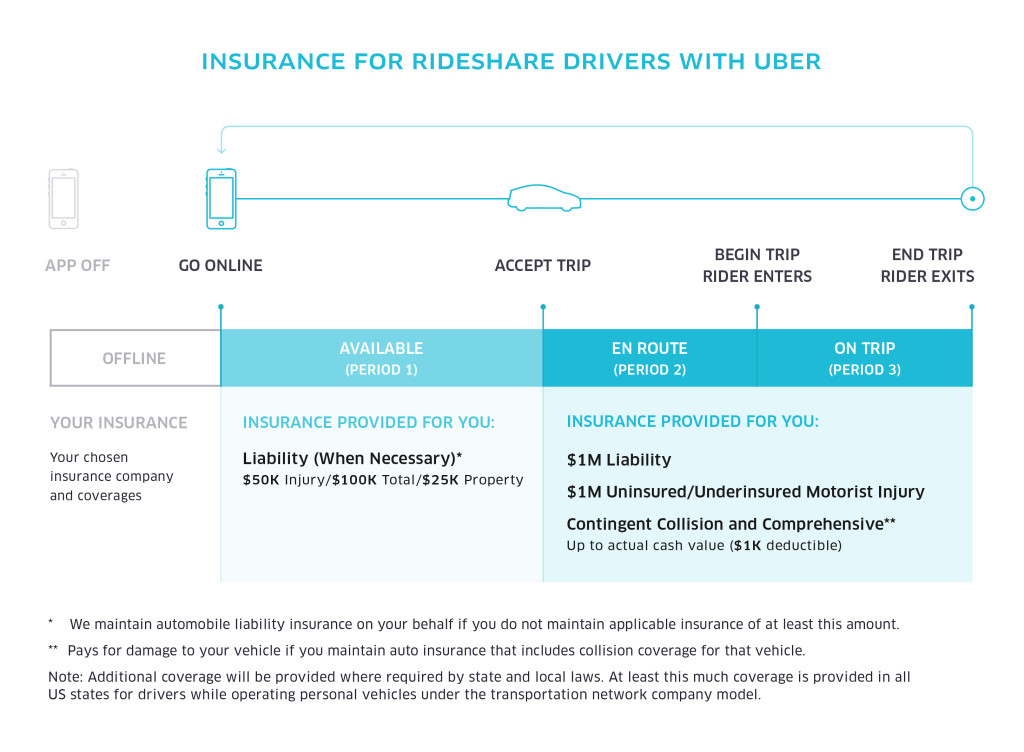

Understanding Uber's Built-In Insurance Coverage

Uber offers a tiered insurance policy that activates depending on your status within the app. When the app is on and you’re waiting for a ride request (Period 1), Uber provides limited liability coverage, often around $50,000 per person, $100,000 per accident for bodily injury, and $25,000 for property damage (known as 50/100/25), along with contingent comprehensive and collision coverage. However, if you already have a personal policy with rideshare coverage, it may serve as the primary insurer during this period.

When you accept a trip and are en route to pick up the passenger (Period 2), Uber increases coverage to at least $1 million in liability, along with full comprehensive and collision. This same level of protection continues while you are actively carrying a passenger (Period 3). It’s crucial to understand these phases so you know when Uber’s insurance steps in and where gaps may exist.

Do You Have To Have Special Insurance To Deliver Food

Do You Have To Have Special Insurance To Deliver FoodMost personal auto insurance policies explicitly exclude coverage for commercial activities, which ridesharing is considered.

If you’re involved in an accident while using the Uber app—even if you haven’t yet picked up a passenger—your personal insurer might deny the claim because you were engaged in a business use of your vehicle. This creates a coverage gap, especially in Period 1 when you’re logged into the app but don’t yet have a ride request.

While Uber does provide contingent coverage during this time, it only activates after your personal insurance denies the claim, which could delay repairs or medical payments. To bridge this gap, many insurers now offer rideshare endorsements that extend your personal policy to cover you when the app is active, ensuring seamless coverage from start to finish.

Several major insurance companies now offer rideshare-specific policies or endorsements that cover drivers throughout all phases of Uber operation.

Does Condo Insurance Cover Special Assessments

Does Condo Insurance Cover Special AssessmentsCompanies like GEICO, State Farm, Allstate, and Progressive provide add-ons that activate coverage during Period 1, when most personal policies fall short. These endorsements typically cost between $5 to $15 extra per month and elevate your existing policy to include protection for both personal and commercial use.

Some drivers, especially those who spend many hours on the road, may consider a commercial auto policy, which offers comprehensive protection but is generally more expensive. It’s important to compare what your current insurer offers, review Uber’s coverage details, and assess your driving frequency to choose the most cost-effective and reliable protection.

| Insurance Period | App Status | Uber Coverage | Personal Insurance Gap? |

|---|---|---|---|

| Period 1 | App on, no trip accepted | Contingent liability: $50/100/25; no collision/comprehensive | Yes – primary coverage often denied |

| Period 2 | En route to passenger | $1 million liability; full collision & comprehensive | No – Uber is primary |

| Period 3 | Transporting passenger | $1 million liability; full collision & comprehensive | No – Uber is primary |

Do I Need Special Insurance for Uber? A Comprehensive Guide

What Insurance Coverage Is Required for Driving With Uber?

Personal Auto Insurance Requirements

- Before driving for Uber, drivers must maintain a personal auto insurance policy that meets the minimum requirements set by their state. This policy is essential because Uber does not provide insurance coverage when the driver is offline or not actively using the app.

- Personal insurance policies typically cover accidents that occur during personal use of the vehicle, such as commuting or running errands. However, most standard policies exclude coverage for commercial activities, which rideshare driving can be considered.

- It’s important for drivers to inform their insurance provider that they are using their vehicle for rideshare services. Some insurers offer rideshare endorsements or specific rideshare policies that extend coverage during different phases of an Uber trip.

Uber’s Provided Insurance Coverage

- When a driver logs into the Uber app and is available to accept rides, Uber provides contingent liability insurance. This coverage kicks in if the driver’s personal insurance does not apply and includes up to $50,000 in bodily injury liability per person, $100,000 per accident, and $25,000 in property damage.

- Once a driver accepts a trip request and is en route to pick up a passenger, Uber’s coverage increases significantly. This period includes up to $1 million in liability coverage, uninsured or underinsured motorist protection, and contingent comprehensive and collision coverage on the driver’s vehicle.

- During the time a passenger is in the vehicle, the same $1 million liability policy remains active, offering the highest level of protection. This ensures that both the driver and passenger are covered for third-party claims in the event of an accident.

Gaps in Coverage and Additional Options

- There are potential coverage gaps, especially during the period between logging into the app and accepting a ride. While Uber provides contingent coverage, drivers may still be liable if a claim exceeds policy limits or involves vehicle damage not covered by the contingent policy.

- To bridge these gaps, many drivers purchase rideshare-specific insurance policies offered by third-party insurers. These policies are designed to seamlessly integrate with both personal insurance and Uber’s coverage, providing continuous protection across all stages of ridesharing.

- Drivers should carefully review the terms of each insurance layer—personal, Uber-provided, and supplemental—to understand exactly when each policy applies. Staying informed helps prevent unexpected out-of-pocket expenses in the event of an accident or claim.

Does driving for Uber affect my personal car insurance rates?

How Ride-Sharing Impacts Personal Car Insurance Coverage

When you drive for Uber, your personal car insurance may not provide coverage during certain periods of your trip, which can expose you to significant financial risk.

Does Special Event Insurance Cover Weather

Does Special Event Insurance Cover WeatherPersonal auto insurance policies are designed for non-commercial use, meaning coverage typically excludes incidents that occur while you're actively working as a rideshare driver. For example, if an accident happens while you're logged into the Uber app waiting for a ride request or while driving a passenger, your personal policy may deny the claim.

This gap in coverage exists because insurers consider driving for hire to increase the risk of accidents due to longer driving hours and unfamiliar routes. As a result, most standard insurance carriers state in their policies that using your vehicle for commercial purposes voids coverage during such periods.

- Personal insurance is structured around the assumption that the vehicle is used for personal, non-commercial trips such as commuting or errands.

- Once you start using your car for Uber, you're engaging in commercial activity, which changes the risk profile in the eyes of insurers.

- Most standard policies explicitly exclude coverage when the vehicle is being used to transport paying passengers, creating coverage gaps.

Does Uber Provide Insurance for Drivers?

Uber does offer some level of insurance coverage for its drivers, but it varies depending on the stage of the rideshare process and is considered secondary or primary only under specific circumstances. Uber's insurance program includes liability, collision, and comprehensive coverage, but the extent of protection depends on whether you're waiting for a ride request, driving to pick up a passenger, or actively transporting a rider.

For instance, when the app is on and you're en route to pick up a rider or have a passenger in the car, Uber provides liability coverage up to certain limits (often $1 million), along with collision and uninsured motorist coverage. However, when you're simply logged into the app with no ride request, Uber may only provide limited liability coverage, which may not be sufficient in an at-fault accident.

How Much Is Special Event Liability Insurance

How Much Is Special Event Liability Insurance- Uber provides contingent liability coverage when you're waiting for a ride request, but it only activates after your personal insurance denies the claim.

- Once a ride is accepted, Uber’s insurance becomes primary, offering higher liability limits and additional protections such as comprehensive and collision coverage.

- Despite these protections, deductibles may apply, and damage to your vehicle might not be fully covered depending on the circumstances of the incident.

Steps to Protect Yourself and Your Insurance Rates

To avoid complications with your personal insurance provider and potential rate increases or policy cancellations, it's essential to inform your insurer if you plan to drive for Uber. Some insurance companies offer rideshare-specific endorsements or policies that bridge the gap between personal and commercial coverage.

These specialized policies maintain consistent protection across all phases of Uber driving and help prevent claim denials. Additionally, disclosing your rideshare activity helps you avoid accusations of misrepresentation, which could lead to your policy being canceled retroactively. Maintaining proper coverage not only safeguards your finances but may also help stabilize your long-term premiums.

- Contact your insurance company to disclose your intention to drive for Uber, as failure to report commercial use could void your policy.

- Ask about adding a rideshare endorsement to your existing policy or switching to a rideshare-specific insurance plan for complete coverage.

- Maintain a clean driving record while driving for Uber, as at-fault accidents or traffic violations can lead to higher premiums even with proper coverage.

Is Uber's optional insurance necessary for drivers?

Understanding Uber's Built-in Insurance Coverage

- Uber provides commercial insurance coverage for its drivers during certain periods of the ride-hailing process, such as when a driver has accepted a ride request or is transporting a passenger.

- This built-in coverage typically includes liability insurance, which protects against damages or injuries the driver may cause to others, as well as contingent comprehensive and collision coverage for damage to the driver’s vehicle.

- However, there are gaps in coverage, especially when the driver is logged into the app but hasn’t yet accepted a ride (Period 1), where Uber only offers limited liability protection and no vehicle damage coverage.

When Optional Insurance Becomes Beneficial

- Drivers who rely heavily on Uber for income may find that the optional insurance, such as through third-party providers or Uber’s own protection plans, helps fill the gaps left by the standard policy.

- This additional coverage can be valuable when a driver’s personal auto insurance doesn’t extend to commercial activities, which could result in denied claims if an accident occurs during rideshare operations.

- Optional insurance often includes protections like personal injury coverage, rental reimbursement, or higher liability limits, giving drivers more comprehensive financial security.

Factors to Consider Before Purchasing Optional Coverage

- Drivers should evaluate how frequently they operate on the Uber platform, as part-time drivers may not need as much supplemental coverage as full-time drivers.

- It's important to review existing personal auto insurance policies to determine what is already covered and where additional protection might be necessary.

- Cost is another key factor; optional insurance adds to the driver’s operating expenses, so weighing the premium costs against potential risks and benefits is essential before making a decision.

Frequently Asked Questions

Do I Need Special Insurance For Uber?

Yes, you need special insurance when driving for Uber. Personal auto insurance typically doesn’t cover you while working as a rideshare driver. Uber provides its own commercial insurance, but it only applies during specific periods of your trip. To stay protected at all times, consider purchasing a rideshare-endorsed policy that covers both personal and commercial use of your vehicle.

When Does Uber’s Insurance Coverage Start?

Uber’s insurance coverage begins when you accept a ride request and ends when the passenger exits the vehicle. During this time, Uber provides liability, uninsured motorist, and collision coverage. However, when the app is on but you haven’t accepted a ride, coverage is limited. Always verify the exact terms in your region, as insurance policies may vary depending on local regulations.

Can I Use My Personal Car Insurance for Uber Driving?

No, you cannot rely solely on personal car insurance when driving for Uber. Most personal policies exclude coverage for commercial activities like ridesharing. If you’re involved in an accident while using the Uber app, your insurer may deny the claim. To avoid gaps in protection, get a rideshare endorsement or switch to a commercial insurance policy designed for Uber drivers.

If you don’t have rideshare insurance and get into an accident while driving for Uber, you could face serious financial consequences. Your personal insurer may refuse to cover damages, leaving you responsible for repairs, medical bills, and legal fees. Uber’s insurance may not cover you during all periods of app usage. Having proper rideshare coverage ensures you’re protected throughout every stage of your ride.

Leave a Reply