How To Sell Life Insurance Policy Quickly And Securely

Selling a life insurance policy can be a practical financial solution for policyholders who no longer need coverage or require immediate funds. Whether due to changing life circumstances, rising premiums, or end-of-life planning, understanding the process is crucial for a quick and secure transaction.

The key lies in knowing your options, such as life settlements, accelerated death benefits, or surrendering the policy to the insurer. Evaluating each choice carefully ensures you maximize value while avoiding potential pitfalls. This guide outlines the essential steps to sell your life insurance policy efficiently and securely, helping you make informed decisions tailored to your financial goals.

How To Sell Your Life Insurance Policy Quickly And Securely

Selling a life insurance policy can be a practical financial decision, especially when premiums are no longer affordable or the policy no longer meets your needs. To do so quickly and securely, it's essential to understand the process of a life settlement, where you sell your policy to a third party for a lump sum payment that’s typically higher than the cash surrender value but less than the death benefit.

Best Life Insurance Rates For Smokers

Best Life Insurance Rates For SmokersThe process begins with evaluating your policy’s eligibility, which generally requires being over 65, holding a policy with a death benefit exceeding $100,000, and no longer needing the coverage for its original purpose. Next, you’ll need to work with reputable life settlement brokers or providers who can connect you with qualified buyers.

Transparency, documentation, and legal compliance are critical to ensure a secure transaction—always request detailed proposals from multiple buyers, review all contractual terms, and consult with a financial or legal advisor before closing the deal. Acting swiftly while maintaining caution throughout verification steps ensures both speed and safety in the sale process.

Understanding Life Settlements: What You Need to Know

A life settlement is a financial transaction in which a policyholder sells their life insurance policy to a third-party investor in exchange for a one-time cash payment.

This option is particularly beneficial for individuals who no longer require the policy’s death benefit or can’t afford premium payments. Unlike surrendering the policy back to the insurer for its cash value, a life settlement typically provides a significantly higher payout. The buyer assumes responsibility for future premiums and receives the death benefit when the original policyholder passes away.

Best Life Insurance Without 2 Year Waiting Period

Best Life Insurance Without 2 Year Waiting PeriodIt’s crucial to understand that life settlements are regulated at the state level, and rules may vary depending on your location—some states require licensing for brokers and mandates for disclosure—so being well-informed about local regulations helps ensure a secure sale. Additionally, the process requires full disclosure of medical and policy information to determine fair market value.

Choosing a Reputable Life Settlement Broker

Selecting a trusted and experienced life settlement broker is one of the most important steps in selling your policy quickly and securely. A qualified broker acts as your advocate, helping you navigate the complexities of the process, obtain competitive offers from multiple buyers, and ensure compliance with legal requirements.

Look for brokers who are licensed, have transparent fee structures, and a strong track record of successful transactions. It's advisable to check their affiliations with industry organizations such as the Life Insurance Settlement Association (LISA) or the Life Insurance Innovation Council (LIIC).

Avoid brokers who demand upfront fees or pressure you to make quick decisions—ethical brokers earn their commission only upon successful completion of the sale. Working with the right professional streamlines the process, increases your chances of receiving top dollar for your policy, and protects you from potential fraud.

New York Life Insurance Company Brokerage General Agency Imo

New York Life Insurance Company Brokerage General Agency ImoRequired Documentation and Evaluation Process

To initiate the sale of your life insurance policy, you must provide comprehensive documentation that allows buyers to accurately assess its value. Essential documents include the original policy contract, recent premium payment records, and complete medical records—especially those related to life expectancy.

Buyers rely on an actuarial review to estimate your life expectancy, which plays a major role in determining the offer you’ll receive. The evaluation process typically involves a HIPAA-compliant medical records service that compiles and submits your health information securely. Insurers and investors use this data to price the risk they’re assuming.

The more complete and accessible your documentation, the faster the underwriting process—and quicker evaluations lead to faster offers and closing. Ensuring accuracy and timeliness in submitting these records can significantly reduce delays.

| Document Type | Purpose | Importance Level |

|---|---|---|

| Life Insurance Policy | Verifies coverage details, death benefit, and ownership | High |

| Medical Records | Used to estimate life expectancy and risk | High |

| Payment History | Confirms policy in good standing | Medium |

| Identification (ID) | Authenticates policyholder identity | Medium |

| Attending Physician Statement (APS) | Provides detailed medical history | High |

How to Sell Your Life Insurance Policy Efficiently and Safely: A Step-by-Step Guide

What challenges make selling life insurance policies quickly and securely difficult?

Online Life Insurance Prices

Online Life Insurance PricesRegulatory and Compliance Requirements

- Life insurance sales are heavily regulated to protect consumers, which means insurers must adhere to strict compliance protocols. These include verifying the identity of applicants, ensuring financial suitability, and complying with anti-money laundering laws, all of which slow down the sales process.

- Each jurisdiction may have different legal frameworks, making it difficult for companies to offer standardized policies across regions. Sales representatives must stay updated on regulatory changes, and any non-compliance can lead to penalties or policy invalidation.

- The underwriting process often requires submitting extensive documentation and waiting for approval from regulatory bodies or internal compliance departments, contributing to delays in finalizing a sale securely.

Complex Underwriting and Risk Assessment

- Unlike other financial products, life insurance requires detailed health and lifestyle evaluations to assess the risk profile of applicants. This involves medical exams, prescription histories, and sometimes lab tests, which extend the time needed to issue a policy.

- Automated underwriting systems have improved speed, but they still cannot handle all cases, especially for applicants with pre-existing conditions or high-risk profiles, which require manual review by underwriters.

- Insurers must balance the need for thorough risk assessment with the pressure to close sales quickly. Rushing this process can lead to inaccurate pricing or undetected risks, undermining the security and sustainability of the policy.

Consumer Hesitation and Lack of Understanding

- Many potential buyers do not fully understand how life insurance works or why they need it, which leads to hesitation and prolonged decision-making. Misconceptions about cost, coverage, and relevance reduce the immediacy of purchasing.

- Life insurance involves discussing death and mortality, topics many people are uncomfortable with, making it emotionally challenging to engage in the sales conversation and commit to a policy.

- Customers often compare multiple offers and delay decisions, especially when faced with complex policy structures such as term vs. permanent insurance. This comparison shopping increases the risk of abandonment before purchase completion.

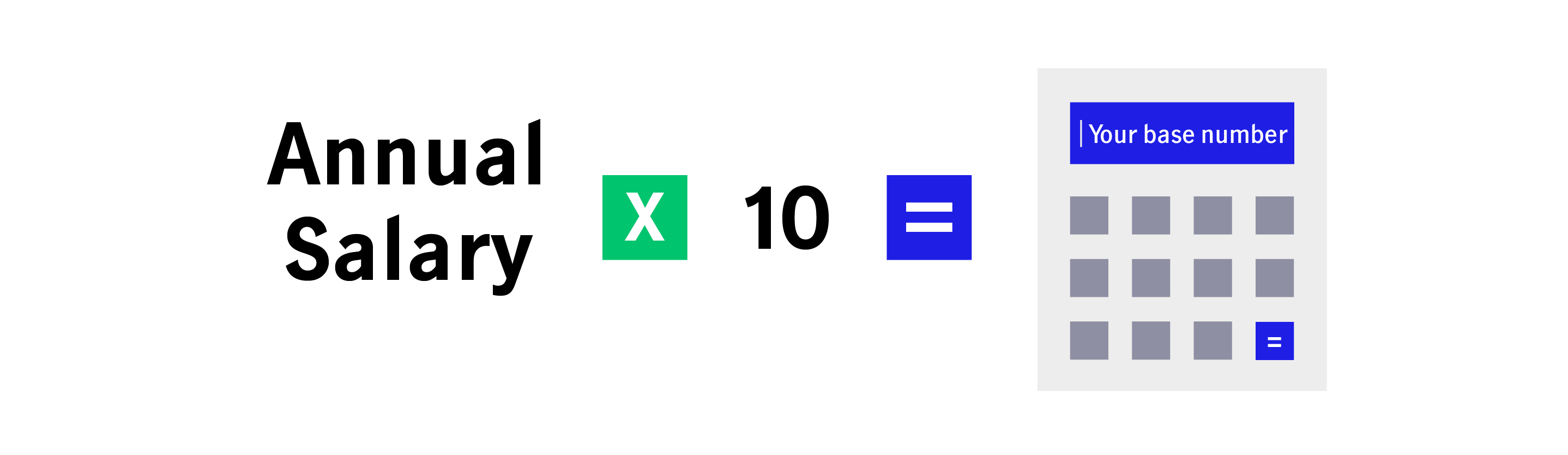

What Is the 10x Rule in Life Insurance and How Does It Impact Policy Sales?

Understanding the 10x Rule in Life Insurance

- The 10x rule in life insurance is a general financial guideline suggesting that an individual should purchase a life insurance policy with a death benefit equal to 10 times their annual income. This rule is intended to ensure that beneficiaries receive sufficient financial support after the policyholder’s death to maintain their standard of living.

- For instance, if someone earns $70,000 per year, the 10x rule would recommend a $700,000 death benefit. This amount aims to cover long-term expenses such as mortgage payments, children’s education, daily living costs, and any outstanding debts.

- While simple to apply, the 10x rule does not account for individual circumstances like existing savings, other sources of income, or specific financial goals, making it a starting point rather than a definitive formula for all individuals.

How the 10x Rule Influences Consumer Decision-Making

- The 10x rule serves as a mental shortcut for consumers who may feel overwhelmed by the complexity of determining appropriate coverage amounts. By providing a clear, easy-to-remember benchmark, it helps individuals initiate the conversation about life insurance needs.

- This rule simplifies the early stages of policy evaluation, giving applicants a baseline figure to discuss with insurance agents or financial advisors. As a result, it reduces decision paralysis and encourages more people to consider purchasing life insurance.

- However, reliance on the 10x rule can sometimes lead to underinsurance or overinsurance if applicants do not adjust the recommendation based on personal variables such as age, health, dependents, or retirement plans.

Impact of the 10x Rule on Life Insurance Sales Strategies

- Insurance agents and companies often use the 10x rule in marketing and sales discussions to quickly illustrate the importance of adequate coverage, making it easier to justify higher policy values during client consultations.

- By anchoring conversations around this rule, agents can guide clients toward larger policies, potentially increasing the commission and overall policy value sold. It adds structure to the sales process and helps establish credibility through a widely recognized guideline.

- Additionally, the 10x rule supports customer education efforts, enabling agents to transition from basic coverage discussions to more comprehensive financial protection plans that include disability, critical illness, or supplemental policies.

Frequently Asked Questions

What Are the First Steps to Sell My Life Insurance Policy Quickly?

To sell your life insurance policy quickly, start by reviewing your policy type and confirming eligibility for a life settlement. Next, gather all necessary documents, including recent statements and medical records. Contact a licensed life settlement broker or provider to get a fair market value estimate. Choosing a reputable company with a fast evaluation process can significantly reduce waiting time and ensure a smoother, more efficient sale.

How Can I Ensure the Sale of My Life Insurance Policy Is Secure?

Ensure a secure sale by working only with licensed, regulated life settlement providers or brokers. Verify their credentials through state insurance departments or industry associations. Use escrow services for fund handling and sign contracts that clearly outline all terms. Avoid sharing sensitive information until legitimacy is confirmed. A transparent process with proper documentation and legal compliance protects your interests and ensures the transaction is both secure and trustworthy.

Who Is Eligible to Sell a Life Insurance Policy?

Typically, individuals aged 65 or older with a policy worth at least $100,000 may qualify to sell their life insurance. Those with serious health conditions often receive higher offers. Eligibility also depends on policy type—whole, universal, or term converted to permanent insurance are most accepted. An evaluation by a life settlement provider will determine qualification based on age, health, and policy details, ensuring only eligible candidates proceed to sale.

Participants Under A Group Life Insurance Plan Are Issued

Participants Under A Group Life Insurance Plan Are IssuedHow Long Does It Take to Receive Money After Selling My Policy?

After selling your life insurance policy, it typically takes 4 to 8 weeks to receive payment. The timeline includes underwriting, appraisals, buyer bidding, and legal approval. Expedited processes may reduce this period slightly. Delays often occur due to incomplete documentation or medical verification. Choosing a trusted provider with a streamlined process helps ensure timely funding once all steps are completed and approvals are secured.

Leave a Reply