Indexed Universal Life Insurance Lawyers

Indexed Universal Life (IUL) insurance offers policyholders the potential for cash value growth tied to market indexes while providing a level of downside protection.

However, complex policy structures, aggressive sales tactics, and misrepresentations can lead to disputes and financial losses. When insurers or agents fail to disclose risks, make unrealistic projections, or breach contractual obligations, policyholders may need legal recourse.

IUL lawyers specialize in navigating these intricate cases, helping clients understand their rights and pursue compensation for misconduct. From reviewing policy terms to litigating bad faith practices, these attorneys play a crucial role in holding financial institutions accountable in the growing IUL insurance landscape.

Business Health Insurance West Virginia

Business Health Insurance West VirginiaWhat You Need to Know About Indexed Universal Life Insurance Lawyers

Indexed Universal Life (IUL) insurance policies are complex financial instruments that combine a death benefit with a cash value component linked to a market index, such as the S&P 500.

While these policies can offer growth potential with downside protection, they are often misunderstood, misrepresented, or improperly sold by agents and financial advisors. This is where Indexed Universal Life Insurance Lawyers come into play. These specialized attorneys represent policyholders who believe they were misled, sold unsuitable policies, or victimized by aggressive sales tactics.

IUL lawyers help clients navigate disputes, file complaints, and pursue legal action when necessary to recover financial losses due to policy mismanagement or fraud. Their expertise is essential in untangling complicated policy terms, fee structures, and insurer misconduct.

Understanding the Role of Indexed Universal Life Insurance Lawyers

Indexed Universal Life Insurance Lawyers specialize in handling legal issues related to the sale, administration, and performance of IUL policies.

Business Insurance Breakout Awards 2025

Business Insurance Breakout Awards 2025These attorneys are well-versed in insurance law, securities regulations, and financial services compliance. They assist clients who were sold policies under false pretenses, such as promises of high returns with little risk, or policies that were unsuitable for their financial goals or risk tolerance.

When misconduct occurs—such as churning, misrepresentation, or failure to disclose risks—IUL lawyers initiate investigations, collect evidence, and represent policyholders in arbitration or court. Their primary goal is to hold insurance companies and financial advisors accountable and to recover financial damages for affected clients.

Common Complaints Addressed by IUL Insurance Attorneys

Clients often turn to IUL lawyers due to a range of issues stemming from improper policy sales or management. Frequent complaints include unexpected premium increases, policies that fail to perform as promised, and excessive fees that erode the policy's cash value.

Some policyholders are sold IULs as long-term retirement solutions despite a lack of income stability to sustain rising premiums. Others are not adequately informed about the complex indexing strategies or how interest credits are capped or buffered.

Business Insurance Checklist

Business Insurance ChecklistIn many cases, financial advisors present IULs as safer alternatives to direct market investments while downplaying surrender charges, loan interest, and the risk of lapse. IUL attorneys analyze these practices to determine whether fiduciary or regulatory standards were breached.

How to Choose the Right IUL Insurance Lawyer

Selecting the right attorney is crucial when challenging an insurance company over an IUL policy dispute. Look for a lawyer or law firm with proven experience in insurance litigation, FINRA arbitration, and cases involving unsuitable financial product sales. A strong IUL lawyer will have a track record of recovering compensation through settlements or verdicts and will offer a free consultation to evaluate your case.

It is also important that they work on a contingency fee basis, meaning they only get paid if you win your case. Effective communication, transparency about the legal process, and familiarity with both insurance regulations and financial planning concepts are key attributes to consider when making your choice.

| Issue | Lawyer’s Role | Outcome Sought |

|---|---|---|

| Misrepresentation of policy benefits | Prove that false claims were made during the sale | Rescission of policy or financial compensation |

| Unsuitability for the client’s financial profile | Establish breach of fiduciary or suitability standards | Recovery of premiums paid and damages |

| Churning or excessive policy replacements | Demonstrate pattern of self-serving transactions | Punitive damages and attorney fees |

| Failure to disclose fees, risks, or caps | Show lack of informed consent | Policy reformation or rescission |

Guidance on Indexed Universal Life Insurance Legal Representation

What are the top-rated Indexed Universal Life insurance companies for legal and financial protection?

Top-Rated Indexed Universal Life Insurance Companies for Legal and Financial Protection

- Northwestern Mutual is consistently ranked among the highest-rated carriers due to its financial strength, long-standing reputation, and strong policyholder protections. The company holds an A++ (Superior) rating from AM Best, indicating exceptional ability to meet ongoing insurance obligations. Its Indexed Universal Life (IUL) policies offer a range of index crediting options with robust death benefit guarantees and contract safeguards, making it a preferred choice for individuals concerned with estate planning and asset protection.

- MassMutual is another top contender recognized for its commitment to policyholder security and transparent product design. With an A++ rating from AM Best and over 170 years in business, MassMutual provides IUL policies that emphasize predictability and long-term value. The company's formalized claims-paying processes and legal compliance protocols enhance policyholder confidence, particularly when managing wealth transfer or creditor protection strategies.

- Guardian Life ranks highly for its customer service, regulatory compliance, and strong performance during economic volatility. Its IUL offerings include features like no-lapse guarantees and multiple index strategy options, all backed by a solid A+ (Superior) financial strength rating from AM Best. Guardian is especially recommended for professionals seeking legal protection for business-owned life insurance and estate liquidity solutions.

Key Legal Protections Offered by Leading IUL Providers

- Policyowners benefit from state-level asset protection laws, which vary in strength but are generally well-supported by insurers like New York Life and Pacific Life. These companies structure their policies to maximize eligibility under exemption statutes, helping shield death benefits and cash values from creditors during lawsuits or bankruptcy proceedings.

- Many top-rated insurers incorporate estate preservation features such as irrevocable beneficiaries and testamentary instructions directly into their IUL contracts. This reduces exposure to probate challenges and ensures smoother inheritance, a critical consideration for high-net-worth individuals aiming to pass wealth efficiently.

- Companies like TIAA and Lincoln Financial emphasize compliance with IRS code sections 7702 and 7702A, ensuring policies maintain their life insurance classification and avoid being reclassified as Modified Endowment Contracts (MECs). This compliance is essential for preserving tax-deferred growth and avoiding premature taxation on withdrawals.

Financial Strength and Stability Metrics for Evaluating IUL Carriers

- AM Best ratings are a primary benchmark for assessing an insurer’s ability to meet policy obligations. Top-tier carriers such as State Farm and Ohio National maintain A+ or higher ratings, reflecting conservative financial management and strong reserves, which directly influence policy security and dividend stability.

- Surplus levels and reserve funding serve as internal financial cushions against market downturns. Leading companies regularly disclose these figures in their annual statements, allowing advisors and clients to evaluate long-term solvency. Firms with higher surplus-to-policy ratios are generally more capable of honoring guarantees during economic stress.

- Longevity in the market—such as with companies like Mutual of Omaha, operating over 100 years—demonstrates resilience through multiple financial cycles. This sustained presence supports policy consistency and reduces the risk of insurer default, a concern for clients using IUL as a foundational element in retirement or legacy planning.

What are the legal risks and drawbacks of indexed universal life insurance?

:max_bytes(150000):strip_icc()/Pros-and-cons-indexed-universal-life-insurance_final-1b83c0fd52154eb69edd47f99ab8927a.png)

Complexity and Misleading Sales Practices

Indexed universal life (IUL) insurance policies are inherently complex financial instruments that combine life insurance coverage with a cash value component tied to the performance of a market index, such as the S&P 500. This complexity can lead to misunderstandings and potential legal exposure when agents or brokers fail to adequately explain how the product works.

- Policyholders may be misled by exaggerated illustrations that project high returns based on favorable market conditions, which often do not account for fees, caps, or negative scenarios, creating a basis for legal claims of misrepresentation.

- Sales agents might understate the cost of insurance, administrative fees, or the impact of policy loans, leading insured individuals to believe the policy is more affordable or effective than it truly is.

- When disclosures are inadequate or omitted, policyholders may sue for fraud or breach of fiduciary duty, especially if the policy lapses prematurely due to unexpected cost increases or poor performance.

Regulatory Scrutiny and Compliance Issues

IUL policies are subject to regulation by state insurance departments and federal securities laws in certain aspects, particularly when indexed features resemble investment products. This dual oversight increases the legal risks for insurers and distributors.

- Regulators, including the Securities and Exchange Commission (SEC) and Financial Industry Regulatory Authority (FINRA), have investigated IUL products for being marketed in ways that blur the line between insurance and securities, potentially requiring broker-dealer registration.

- Insurance companies may face enforcement actions if their marketing materials or agent scripts are found to contain misleading comparisons, such as favorably stacking IUL against other retirement savings vehicles without disclosing inherent risks.

- Non-compliance with disclosure requirements, such as failure to clearly explain caps, participation rates, or reset frequencies, can result in fines, consumer restitution, or reputational damage for financial institutions.

Performance Volatility and Contractual Limitations

Although IUL policies offer the potential for higher returns than traditional universal life insurance by linking cash value growth to indexed performance, they are subject to structural constraints that can diminish returns and pose legal challenges.

- Insurance companies apply caps, spreads, and participation rates that limit upside potential, and these mechanisms can be adjusted annually, leading to disputes if policyholders feel returns are unfairly restricted despite strong index performance.

- The guarantees provided, such as a floor of 0% during market downturns, do not eliminate the risk of insufficient cash value accumulation, especially if premiums are based on optimistic projections that later prove unsustainable.

- If policyholders must pay additional out-of-pocket premiums to keep the policy in force due to lower-than-expected performance, they may claim the product was unsuitable for their financial situation, opening the door to legal action based on suitability standards.

What legal considerations should indexed universal life insurance lawyers address when selling IUL policies?

Fulfillment of Fiduciary and Regulatory Duties

- Lawyers involved in the sale or structuring of Indexed Universal Life (IUL) insurance policies must ensure strict compliance with fiduciary obligations, particularly when advising clients on complex financial products. They are expected to act in the client's best interest, providing advice that aligns with the client’s financial goals, risk tolerance, and long-term needs.

- Compliance with state insurance laws and federal securities regulations is critical. Although IUL policies are life insurance products, they often contain investment-like features tied to market indices, which may trigger scrutiny under both insurance codes and, in some cases, securities laws—especially if the policies are marketed as investment vehicles.

- Legal professionals must also verify that insurance agents and brokers are properly licensed and that all marketing materials adhere to regulatory standards set by entities such as the National Association of Insurance Commissioners (NAIC) and state insurance departments. Misrepresentation or omission in policy illustrations can lead to regulatory penalties and civil liability.

Adequate Disclosure and Avoidance of Misrepresentation

- Lawyers must ensure that all communications regarding IUL policies include clear, accurate disclosures about the nature of index crediting methods, cap rates, participation rates, and potential fees. Overstating potential returns or understating the impact of caps and spreads can constitute grounds for legal action if clients suffer financial loss due to misleading information.

- Policy illustrations used in sales must be realistic and not based on hypothetical maximum returns. Regulatory bodies require that illustrated scenarios include conservative, moderate, and optimistic projections, and lawyers should review these for compliance to avoid deceptive sales practices claims.

- Attorneys should emphasize the distinction between the policy's death benefit, cash value growth, and premium payments, ensuring clients understand that IULs are not guaranteed to perform like traditional investments and that lapses can occur if premiums are not maintained according to the policy’s requirements.

Compliance with Suitability and Replacement Requirements

- When an IUL is being sold as a replacement for an existing life insurance policy, lawyers must ensure adherence to mandatory replacement regulations. This includes the completion of detailed replacement forms, written client consent, and notification to the current insurer, as required by state insurance laws.

- Suitability analysis is a key legal consideration. Lawyers should confirm that insurers and agents have conducted a thorough assessment of the client’s financial situation, insurance needs, and retirement objectives before recommending an IUL. Failure to establish suitability can result in regulatory censure or litigation.

- Documentation of the sales process, including client interviews, risk disclosures, and suitability determinations, should be preserved. In the event of a dispute, comprehensive records can demonstrate that legal and regulatory standards were followed during the policy sale.

Frequently Asked Questions

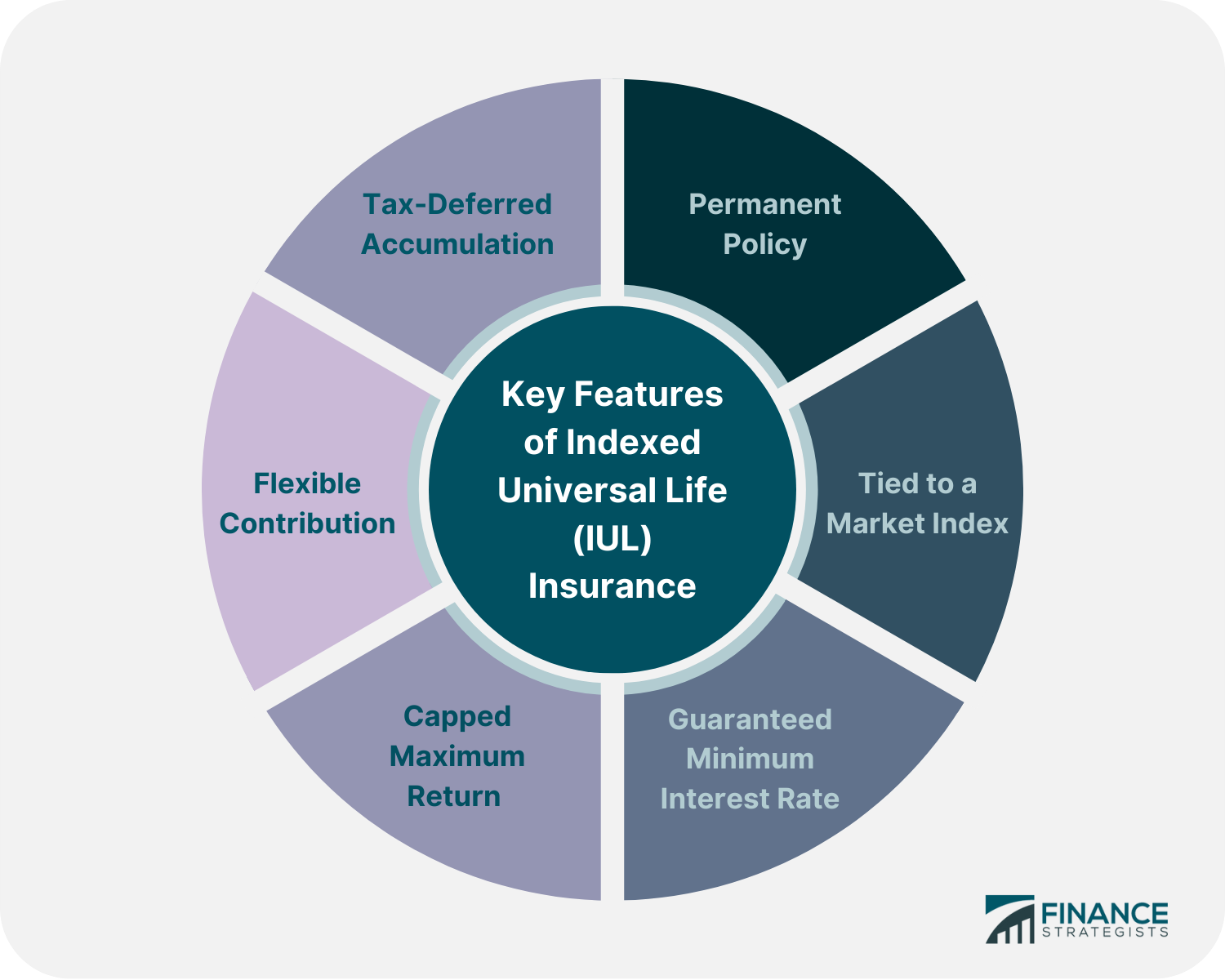

What Is Indexed Universal Life Insurance?

Indexed Universal Life (IUL) insurance is a type of permanent life insurance that offers both a death benefit and a cash value component. The cash value grows based on the performance of a stock market index, such as the S&P 500. It provides flexibility in premiums and death benefits, with protection against market losses due to guaranteed minimum interest rates.

Why Would I Need a Lawyer for Indexed Universal Life Insurance?

You may need a lawyer for Indexed Universal Life Insurance if you suspect misrepresentation, fraud, or bad faith practices by the insurer or agent. Legal counsel can help review policy terms, uncover misleading sales tactics, and pursue claims for wrongful denials or excessive fees. An experienced attorney ensures your rights are protected and can assist in resolving disputes through negotiation or litigation.

Can I Sue My Insurance Company for IUL Policy Mismanagement?

Yes, you can sue your insurance company for mismanaging your IUL policy if there is evidence of negligence, deceptive sales practices, or breach of contract. Common grounds include failure to disclose risks, inadequate funding illustrations, or improper administration. A qualified lawyer can assess your case, gather evidence, and file a lawsuit to recover financial losses or seek policy corrections through the legal system.

How Do I Choose the Right Lawyer for IUL Insurance Issues?

Choose a lawyer with specific experience in life insurance disputes, particularly IUL policies. Look for a proven track record in handling bad faith claims, policy reviews, and insurance litigation. Check client reviews, professional credentials, and firm reputation. Schedule consultations to assess communication style and expertise. The right attorney should clearly explain your legal options and offer a transparent fee structure.

Leave a Reply