Tiaa Final Expense Life Insurance Reviews

Tiaa Final Expense Life Insurance is designed to provide financial protection for end-of-life costs, offering peace of mind to policyholders and their families.

This type of whole life insurance is tailored for seniors, typically aged 50 to 85, seeking affordable coverage without a medical exam. Tiaa, known for its focus on financial security, offers straightforward policies with guaranteed acceptance and fixed premiums. Reviews highlight the ease of application, reliable customer service, and transparent terms.

While some note higher premiums compared to competitors, many appreciate the no-hassle underwriting process. This article explores real customer experiences, policy benefits, and key considerations when evaluating Tiaa’s final expense insurance as part of long-term financial planning.

Term And Whole Life Insurance Difference

Term And Whole Life Insurance DifferenceTiaa Final Expense Life Insurance Reviews: What Customers Are Saying

TIAA Final Expense Life Insurance is a type of whole life insurance specifically designed to cover end-of-life costs such as funeral expenses, medical bills, and other outstanding debts.

Reviews of this policy generally reflect appreciation for its straightforward application process, fixed premiums, and the financial security it offers to beneficiaries. Many policyholders highlight that TIAA, known primarily for its retirement services, brings a sense of reliability and trust to its life insurance offerings.

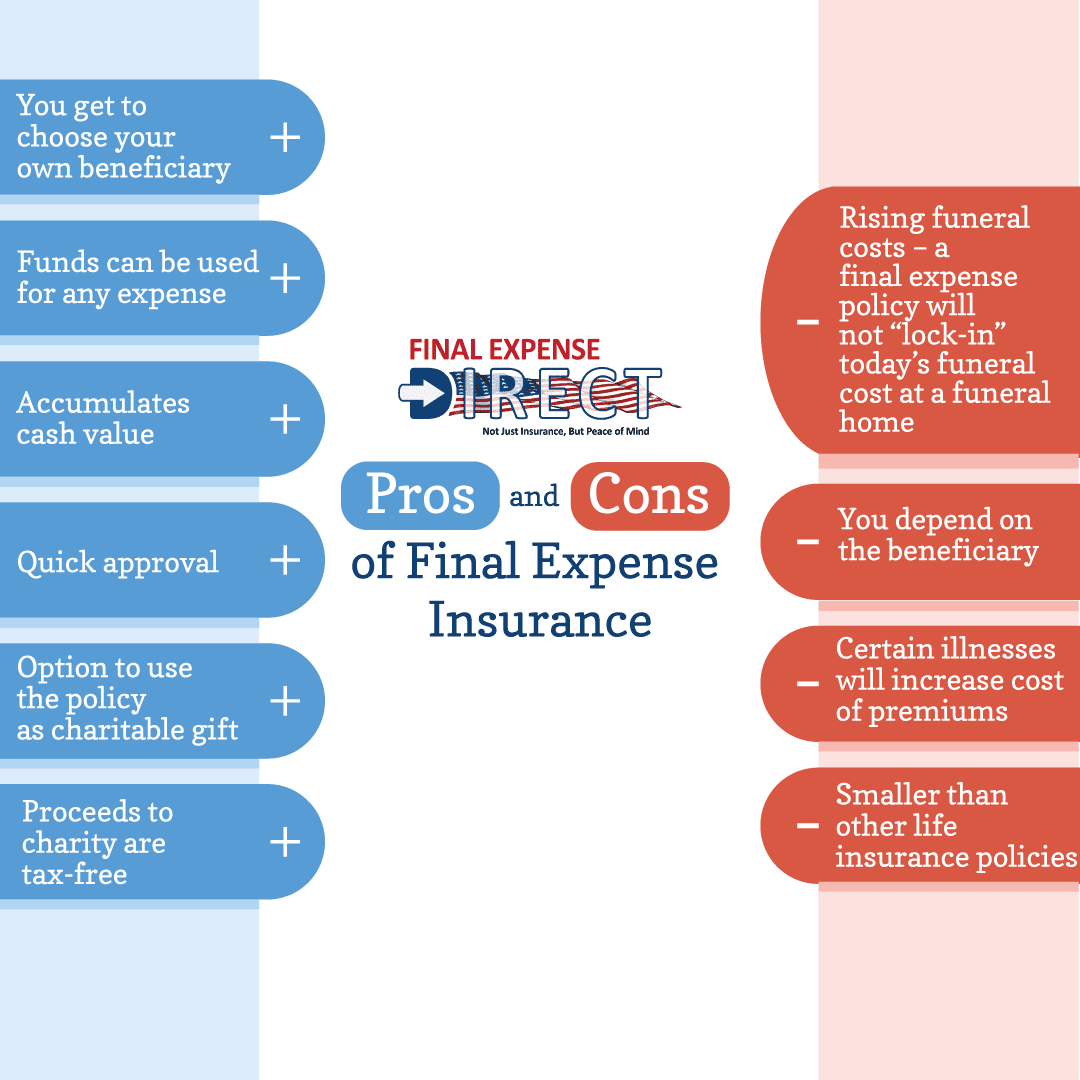

Customers often praise the policy’s ease of qualification, which typically does not require a medical exam, making it accessible for seniors aged 50 to 85. However, some reviews note that coverage amounts are relatively modest—usually ranging from $5,000 to $40,000—which may not fully cover all final expenses in high-cost areas.

Additionally, while premiums are fixed and will not increase over time, they may be higher compared to similar products in the market, depending on age and health at enrollment. Overall, TIAA Final Expense Life Insurance is viewed as a dependable option for individuals seeking peace of mind through simplified underwriting and lifelong coverage.

Term Life Insurance Quotes Gilbert

Term Life Insurance Quotes GilbertKey Benefits of Tiaa Final Expense Life Insurance

One of the main advantages of TIAA Final Expense Life Insurance is its guaranteed acceptance for individuals within the eligible age range, which eliminates the need for a medical exam or extensive health questions. This makes the policy especially appealing to older adults who may have pre-existing conditions that could disqualify them from traditional life insurance.

Another significant benefit is the level premiums, which remain constant throughout the life of the policy, protecting policyholders from future rate hikes. The death benefit is paid directly to beneficiaries and can be used for any purpose, although it is typically intended to cover funeral costs, medical bills, or outstanding debts.

Additionally, because TIAA is a reputable financial institution with strong ratings from agencies like AM Best, customers often feel confident in the company’s ability to honor claims and provide reliable service. These features collectively make the policy a practical financial tool for end-of-life planning.

How Tiaa Final Expense Life Insurance Compares to Competitors

When evaluating TIAA Final Expense Life Insurance alongside similar products from companies like AIG, Colonial Penn, or Mutual of Omaha, several differentiating factors emerge. While many final expense policies offer guaranteed issue and simplified underwriting, TIAA stands out due to its association with financial stability and customer service reputation.

Terms For Life Insurance

Terms For Life InsuranceHowever, some competitors offer lower premiums for the same coverage amounts or allow for higher maximum benefits—sometimes up to $50,000 or more. TIAA’s maximum coverage of $40,000 may be limiting for those seeking more comprehensive protection. Another point of comparison is policy flexibility; while TIAA provides consistent, no-frills coverage, other insurers may include options like graded death benefits or return-of-premium riders.

That said, TIAA’s transparent pricing and direct support model can be preferable for customers who value clarity over bells and whistles. Ultimately, the decision often comes down to balancing coverage limits, cost, and personal financial goals.

Understanding the Coverage and Costs

TIAA Final Expense Life Insurance offers whole life coverage with fixed premiums based on age, gender, and selected death benefit at the time of enrollment.

Coverage amounts start at $5,000 and go up to $40,000, allowing policyholders to choose a level that aligns with their anticipated end-of-life expenses. Premiums can range from approximately $20 to over $100 per month, depending on these factors—older applicants will face higher rates.

It's important to note that the policy includes a two-year waiting period for full death benefits; if the insured passes away within this period due to natural causes, beneficiaries typically receive a return of premiums plus interest, rather than the full benefit. This is a common feature in guaranteed issue policies and serves to mitigate risk for the insurer. Below is a sample breakdown of potential costs and coverage based on age and gender:

| Age & Gender | Coverage Amount | Monthly Premium |

|---|---|---|

| 55-year-old Female | $10,000 | $22 |

| 65-year-old Male | $20,000 | $48 |

| 75-year-old Female | $30,000 | $89 |

| 80-year-old Male | $40,000 | $135 |

These estimates illustrate how premiums increase significantly with age, emphasizing the advantage of enrolling earlier. Despite the waiting period and moderate coverage limits, many customers consider TIAA’s pricing fair given the no medical exam requirement and the insurer’s strong financial backing.

Tiaa Final Expense Life Insurance Reviews: A Comprehensive Guide

What are the key features and reviews of TIAA final expense life insurance?

Key Features of TIAA Final Expense Life Insurance

TIAA Final Expense Life Insurance is designed to provide financial support to cover end-of-life costs such as funeral expenses, medical bills, and other outstanding debts.

One of its primary advantages is that it offers guaranteed acceptance for individuals within a specified age range, usually between 50 and 80 years old, without requiring a medical exam or health questionnaire. The policy comes with level premiums that remain constant over time, which helps with long-term financial planning.

Additionally, TIAA offers a range of death benefit options, typically from $10,000 up to $40,000, allowing policyholders to select coverage that suits their needs. The entire application process is streamlined and can often be completed over the phone, making it accessible and convenient.

- Guaranteed acceptance for applicants aged 50–80, regardless of health condition

- No medical exam or health questions required during application

- Fixed death benefit options from $10,000 to $40,000 with level premiums

Customer Reviews and User Experience

Customer feedback on TIAA’s final expense life insurance reflects a mix of positive and neutral experiences. Many policyholders appreciate the simplicity and ease of the application process, noting that customer service representatives are typically knowledgeable and patient.

Online reviews often highlight the trustworthiness of TIAA as a well-established financial institution with a strong reputation in retirement services. However, some customers have mentioned that premiums can be relatively higher compared to similar policies from other insurers, especially for older applicants.

Others report delays in claim processing or difficulty in reaching support teams during peak times. Despite these concerns, overall satisfaction tends to be moderate to high, particularly among those who value no medical underwriting.

- Positive feedback on customer service and ease of enrollment

- Some complaints about premium costs for older age groups

- Occasional delays reported in claims handling and support response times

Coverage Options and Policy Flexibility

TIAA Final Expense Life Insurance offers limited but straightforward coverage focused specifically on end-of-life expenses.

The policy is a whole life insurance product, meaning it accumulates no cash value beyond the death benefit and remains in force for the insured’s lifetime as long as premiums are paid. While customization options are minimal compared to more comprehensive life insurance policies, this simplicity appeals to individuals looking for a no-frills solution.

Beneficiaries receive the full death benefit as long as the policy is active, and there are no investment components or complex riders to manage. This makes it especially suitable for seniors who want to ensure their loved ones are not burdened with funeral and administrative costs.

- Whole life coverage with lifetime protection and fixed premiums

- Limited customization but focused on essential end-of-life expense coverage

- No cash value accumulation or investment features, emphasizing simplicity

What are the concerns surrounding TIAA final expense life insurance?

Limited Coverage Amounts and Inflation Risk

- TIAA final expense life insurance policies typically offer lower death benefits, often ranging from $5,000 to $25,000, which may not be sufficient to cover rising funeral and end-of-life costs over time.

- With inflation steadily increasing the cost of living and medical services, the fixed payout from a final expense policy may lose purchasing power by the time it is needed.

- Policyholders might underestimate future expenses, leading to out-of-pocket costs for families despite having insurance in place.

- TIAA’s final expense plans generally charge higher premiums compared to their actual death benefit, particularly for older applicants or those with health conditions.

- Because these are often guaranteed issue policies with no medical exam, the elevated premiums reflect the insurer’s increased risk, resulting in a less cost-effective long-term value.

- Consumers may find that, over decades of payments, they pay more in premiums than the policy ultimately pays out, reducing its financial benefit.

Lack of Flexibility and Investment Options

- Unlike some permanent life insurance policies that build cash value or offer investment components, TIAA final expense insurance is typically a simple whole life product with minimal flexibility.

- Policyholders cannot borrow against the policy, withdraw cash value, or adjust their coverage easily as financial needs change.

- The rigid structure limits its utility beyond covering immediate end-of-life expenses, making it less versatile compared to broader life insurance alternatives.

What does the 10-year rule mean for TIAA final expense life insurance policies?

The 10-year rule in the context of TIAA final expense life insurance policies refers to a specific provision that governs the early surrender or cancellation of the policy.

This rule is designed to protect the insurer from financial losses that may occur when policyholders withdraw from their plans shortly after issuance, especially when the costs of underwriting and issuing the policy have not yet been recouped. Under the 10-year rule, policyholders may face significant surrender charges or penalties if they cancel their policy within the first 10 years of coverage.

These charges typically decrease over time and may eventually disappear after the 10-year period ends. It’s important for policyholders to fully understand how and when these charges apply, as they can substantially reduce the cash surrender value they receive.

What Are the Financial Implications of the 10-Year Rule?

- The primary financial implication of the 10-year rule is the imposition of surrender charges if the policy is terminated early. These charges are usually a percentage of the cash value and are highest in the first few years of the policy, gradually declining each year until they reach zero after the 10-year mark.

- Policyholders who need to access their funds during the early policy years may find their liquidity significantly restricted due to these penalties. This can impact decisions related to financial planning, especially in times of urgent need.

- Understanding the schedule of surrender fees allows individuals to make informed decisions about whether to maintain, borrow against, or surrender the policy. Reviewing the policy’s schedule of charges, typically located in the contract, is critical for long-term financial strategy.

How Does the 10-Year Rule Affect Cash Value Accumulation?

- Final expense life insurance policies from TIAA often build cash value over time, but the 10-year rule can influence how much of that value is accessible during the early years. A portion of premiums pays for administrative costs and insurance charges, which slows the initial growth of cash value.

- Because surrender charges apply during the first decade, the amount a policyholder receives upon surrendering can be much lower than the total premiums paid, especially in years one through five. This discrepancy often surprises new policyholders.

- After the 10-year period, the cash value becomes more liquid and accessible with minimal or no fees. Long-term retention of the policy not only avoids penalties but also allows the cash value to grow more efficiently, which can be used for loans or withdrawals later in life.

Are There Exceptions or Alternatives to the 10-Year Rule?

- TIAA may offer limited exceptions to the 10-year surrender rule in cases of financial hardship, terminal illness, or other extenuating circumstances. These are assessed on a case-by-case basis and require documentation.

- Policyholders have the option to take policy loans instead of surrendering the policy, which allows them to access cash value without triggering surrender charges. However, unpaid loans reduce the death benefit and may affect the policy’s longevity.

- Some TIAA policies may offer riders or alternative structures with different surrender timelines. It is advisable to compare policy options during underwriting to select a plan that aligns with anticipated financial needs and access to funds.

Frequently Asked Questions

What is TIAA Final Expense Life Insurance?

TIAA Final Expense Life Insurance is a simplified whole life policy designed to cover end-of-life costs such as funeral expenses, medical bills, and outstanding debts. It offers guaranteed acceptance for eligible individuals aged 50–85 without a medical exam. The policy builds cash value over time and provides a fixed death benefit to beneficiaries, helping ease financial burdens after the policyholder’s passing.

How much does TIAA final expense insurance cost?

Monthly premiums for TIAA Final Expense Life Insurance vary based on age, gender, and coverage amount, typically ranging from $30 to $150. Since it’s a simplified issue policy, pricing is generally higher than traditional life insurance due to guaranteed acceptance and no medical exam. You can choose coverage from $7,500 to $50,000, and premiums remain level for life once the policy is issued.

Does TIAA final expense insurance require a medical exam?

No, TIAA Final Expense Life Insurance does not require a medical exam. It uses a simplified underwriting process with a few health-related questions. Most applicants qualify regardless of health conditions, making it ideal for those who may be declined for other life insurance policies. Approval is typically fast, and coverage begins shortly after application approval and the first premium payment.

Can I cancel my TIAA final expense policy at any time?

Yes, you can cancel your TIAA Final Expense Life Insurance policy at any time by contacting customer service or stopping premium payments. If canceled, you may receive a surrender value based on the policy’s cash value, minus any fees. However, letting the policy lapse ends coverage and forfeits any future death benefit, so consider alternatives like a reduced paid-up option.

Leave a Reply