Can You Put A Life Insurance Policy In A Trust

Placing a life insurance policy in a trust is a strategic financial move that can offer significant benefits for estate planning and wealth transfer.

By assigning a policy to a trust, particularly an irrevocable life insurance trust (ILIT), individuals can potentially remove the death benefit from their taxable estate, reducing estate taxes for heirs. This approach also provides greater control over how and when beneficiaries receive proceeds, offering protection against creditors and poor financial decisions.

While the process involves legal and financial considerations, including surrendering certain rights to the policy, the long-term advantages often outweigh the complexities for those with sizable estates or specific inheritance goals.

How To Purchase Workers Compensation Insurance Online For Business

How To Purchase Workers Compensation Insurance Online For BusinessCan You Put a Life Insurance Policy in a Trust?

Yes, you can place a life insurance policy in a trust, and doing so is a common estate planning strategy used to maintain control over how the death benefit is distributed, potentially reduce or eliminate estate taxes, and protect the proceeds from creditors.

Placing a life insurance policy in an irrevocable life insurance trust (ILIT) transfers ownership of the policy to the trust, which helps remove the death benefit from the insured’s taxable estate. This can be especially valuable for individuals with large estates who might otherwise face substantial estate tax liabilities.

Additionally, this structure allows the insured to specify precise instructions on how and when beneficiaries receive funds, which is particularly useful for supporting minors or managing spendthrift concerns.

What Is an Irrevocable Life Insurance Trust (ILIT)?

An irrevocable life insurance trust (ILIT) is a legal entity specifically designed to own one or more life insurance policies.

Insurance Brokers Business

Insurance Brokers BusinessOnce established, the trust becomes the policy’s owner and beneficiary, and the terms of the trust cannot be changed or revoked without the consent of the beneficiaries. This irrevocability makes the policy and its death benefit independent of the insured’s estate, which helps shield it from estate taxes and creditor claims.

The trustee manages the trust according to the grantor’s instructions, ensuring that the proceeds are distributed according to predetermined terms, such as when a child reaches a certain age or for specific purposes like education or healthcare.

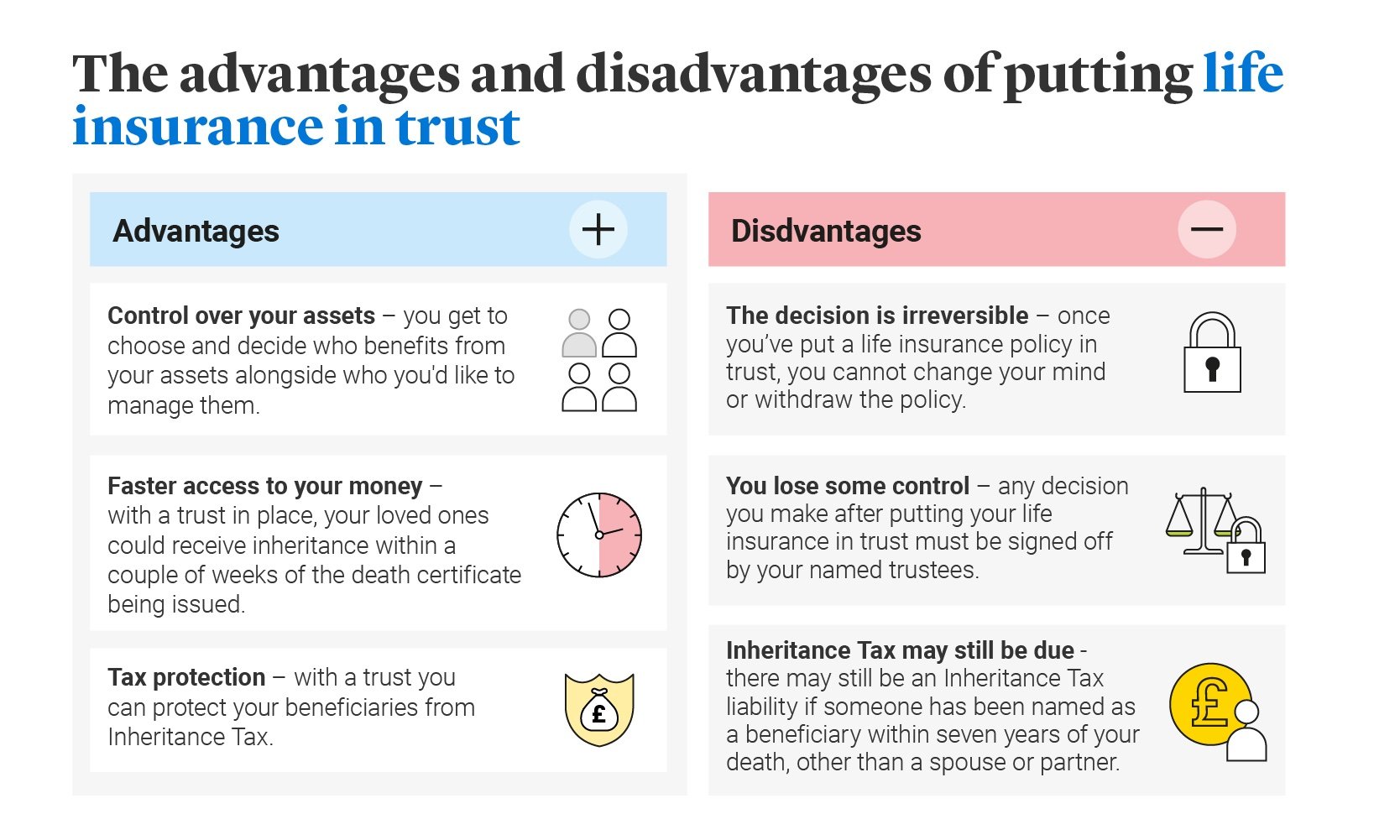

Advantages of Placing Life Insurance in a Trust

Placing a life insurance policy in a trust offers several key advantages. First, it can prevent estate taxes by removing the death benefit from the insured’s taxable estate, which is crucial when the combined value of assets exceeds the federal estate tax exemption threshold.

Second, it provides greater control over distribution, allowing the grantor to set conditions for how and when beneficiaries receive the funds, which helps protect irresponsible or underage heirs.

Insurance Business Architecture

Insurance Business ArchitectureThird, the trust can protect assets from creditors and legal claims, ensuring the proceeds are preserved for their intended beneficiaries. Moreover, transferring the policy to an ILIT can streamline the estate settlement process, avoiding probate and potentially delivering funds to beneficiaries more quickly.

How to Transfer a Life Insurance Policy to a Trust

Transferring a life insurance policy to a trust involves several important steps to ensure the process is valid and achieves its intended purposes. First, the grantor must create an irrevocable life insurance trust and appoint a trustee—typically someone independent, like a professional trustee or family member who is not a beneficiary.

Then, the policy is transferred from the individual owner to the trust, a process known as an assignment. The insured must survive this transfer by at least three years for the policy to be fully excluded from the estate under federal tax rules.

During this period, the trust must have enough funds to pay premiums, often facilitated through the annual gift tax exclusion by sending funds to the trust beneficiaries who then gift them back to the trust (known as the Crummey powers). Proper documentation and legal oversight are essential to ensure compliance with IRS regulations.

| Benefit | Description | Relevance |

|---|---|---|

| Estate Tax Reduction | Removes the death benefit from the taxable estate. | Crucial for estates exceeding exemption limits. |

| Controlled Distribution | Allows specific instructions for disbursement to beneficiaries. | Ideal for minors or financially inexperienced heirs. |

| Creditor Protection | Shields proceeds from legal claims and debts. | Preserves funds for intended use. |

| Probate Avoidance | Speeds up payout by bypassing court processes. | Ensures quicker access to funds for beneficiaries. |

| Irrevocable Structure | Ensures permanence and tax advantages. | Requires careful planning and professional guidance. |

How to Place a Life Insurance Policy in a Trust: A Comprehensive Guide

Should you place your life insurance policy in a trust for better estate planning?

What Is a Life Insurance Trust and How Does It Work?

- A life insurance trust, commonly known as an irrevocable life insurance trust (ILIT), is a legal entity designed to own a life insurance policy. When you transfer your policy to an ILIT, the trust becomes the policy's owner and beneficiary, meaning it receives the death benefit upon your passing.

- The trust is established with specific instructions outlining how and when the proceeds should be distributed to your beneficiaries. This structure allows you to maintain control over how funds are used, even after your death, which can be particularly important if beneficiaries are minors or lack financial experience.

- Because the trust is typically irrevocable, you generally cannot change its terms or reclaim ownership of the policy once it’s transferred. This permanence is key to gaining certain tax and estate planning advantages, as it removes the policy from your taxable estate.

Can a Trust Help Reduce Estate Taxes?

- If your estate exceeds the federal estate tax exemption threshold—currently $12.92 million for an individual in 2024—the death benefit from a life insurance policy owned by you is included in your taxable estate. Placing the policy in an ILIT removes it from your estate, potentially reducing or eliminating estate tax liability.

- For high-net-worth individuals, this tax-saving strategy can preserve significantly more wealth for heirs. Without a trust, estate taxes could force beneficiaries to liquidate other assets to cover the tax bill, disrupting your overall estate plan.

- It’s important to note that to achieve these tax benefits, the transfer of the policy to the trust must comply with federal gift tax rules. For example, if you transfer an existing policy into an ILIT, the transfer may be considered a taxable gift if you die within three years of the transfer.

How Does a Trust Enhance Control and Flexibility?

- By using a trust, you can set detailed distribution rules for the life insurance proceeds, preventing beneficiaries from receiving a large sum of money all at once. Instead, you can specify periodic payments, fund usage for education or healthcare, or conditions based on age or milestones.

- A trust can also protect the proceeds from creditors, divorce settlements, or poor financial decisions by beneficiaries. This layer of asset protection is especially valuable when beneficiaries have unstable financial situations or are vulnerable to outside claims.

- Additionally, a trust allows you to name successor trustees—individuals or institutions who manage the trust after your death. This ensures professional or trusted oversight of the funds, maintaining the integrity of your estate planning goals over time.

What Are the Benefits of Placing a Life Insurance Policy in a Trust?

Estate Tax Minimization

- Placing a life insurance policy in an irrevocable life insurance trust (ILIT) removes the death benefit from the insured’s taxable estate, potentially reducing or eliminating federal estate tax liability.

- Because the trust, not the individual, owns the policy, the proceeds are not included when calculating the total value of the estate for tax purposes, which is particularly beneficial for high-net-worth individuals.

- This strategy is effective in preserving more of the inheritance for beneficiaries, especially in estates that exceed the federal estate tax exemption threshold, currently set at several million dollars depending on the tax year.

Control Over Distribution of Proceeds

- When a life insurance policy is held in a trust, the grantor can specify detailed instructions for how and when the benefits are distributed to beneficiaries.

- For example, funds can be released in staged distributions, such as when beneficiaries reach certain ages or achieve specific milestones like graduation or marriage.

- This helps prevent beneficiaries from receiving large sums of money all at once, which can be mismanaged, and ensures long-term financial security according to the grantor’s wishes.

Asset Protection and Creditor Safeguarding

- Life insurance proceeds held within a properly structured trust can be protected from creditors, lawsuits, and bankruptcy claims against the beneficiaries.

- Since the trust legally owns the policy and controls disbursement, the funds are not considered direct assets of the beneficiary, making them less accessible to legal judgments.

- This protection is especially valuable for beneficiaries in high-risk professions or those who may face future financial difficulties, ensuring that the intended support is preserved.

Frequently Asked Questions

Can you place a life insurance policy in a trust?

Yes, you can place a life insurance policy in a trust, typically a revocable or irrevocable life insurance trust (ILIT). Doing so allows you to remove the policy from your taxable estate, potentially reducing estate taxes. The trust becomes the policy owner and beneficiary, providing control over how proceeds are distributed to heirs, ensuring privacy and protection from creditors.

What are the benefits of putting life insurance in a trust?

Putting life insurance in a trust helps avoid estate taxes by removing the policy from your taxable estate. It offers control over how and when beneficiaries receive funds, protects assets from creditors, and ensures privacy since trusts aren’t public like wills. An insurance trust can also help manage proceeds for minor children or beneficiaries who may not handle large sums responsibly.

What type of trust is best for holding life insurance?

An irrevocable life insurance trust (ILIT) is typically the best choice for holding life insurance. It removes the policy from your taxable estate, minimizing estate taxes. Once established, you can't change the terms, ensuring assets are protected. The ILIT owns and benefits from the policy, giving you control over distribution while offering financial protection and privacy for beneficiaries.

Does placing life insurance in a trust affect the death benefit?

No, placing life insurance in a trust does not reduce the policy’s death benefit. The full amount is paid to the trust when the insured dies. The trust then distributes funds according to its terms. While the death benefit remains unchanged, structuring the policy within a trust can help avoid estate taxes, ensuring more of the benefit reaches your intended beneficiaries efficiently.

Leave a Reply