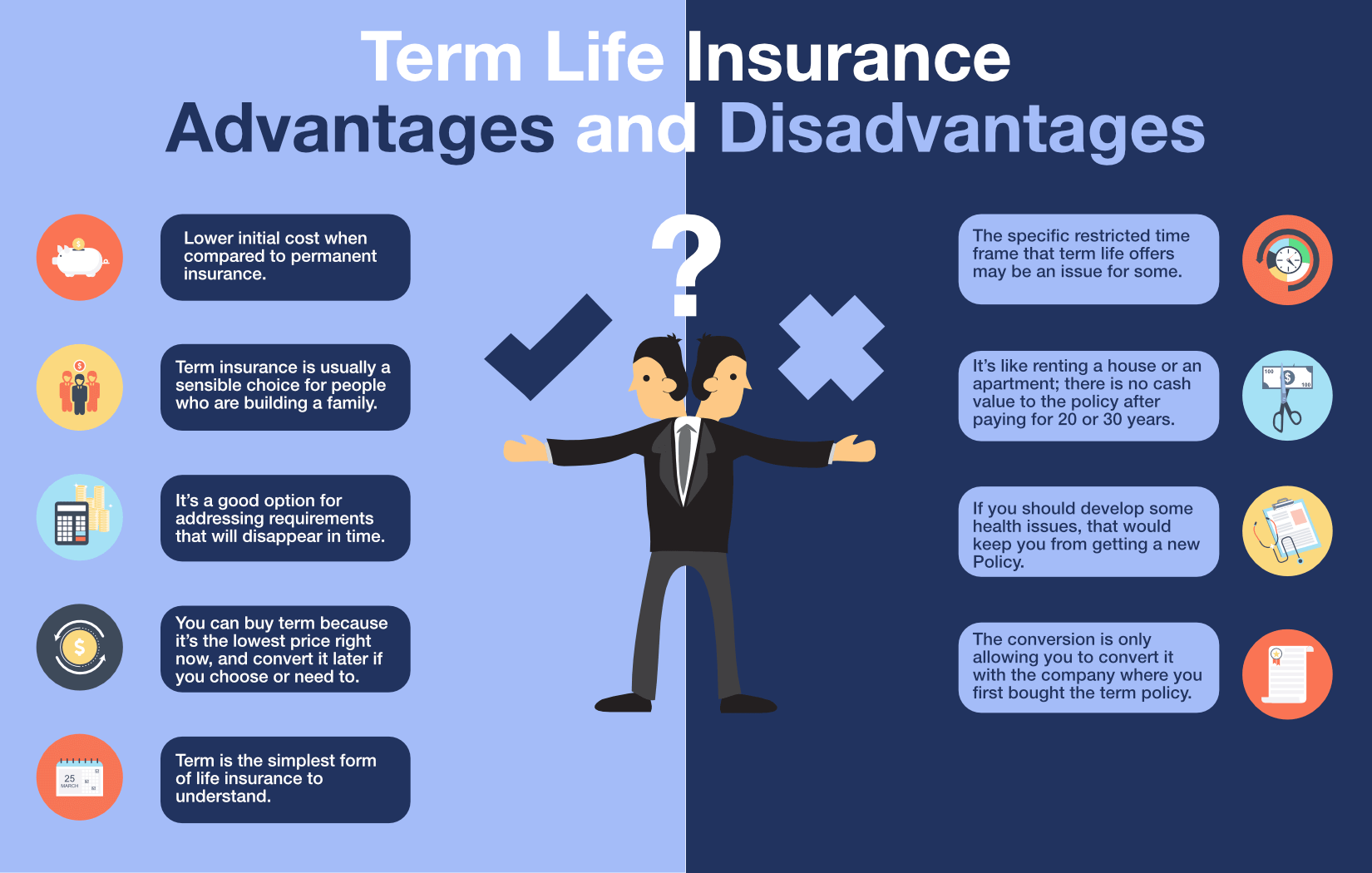

Drawbacks Of Term Life Insurance

Term life insurance is often praised for its affordability and simplicity, making it a popular choice for individuals seeking temporary coverage.

However, despite its benefits, it comes with notable drawbacks that potential policyholders should consider. Unlike permanent life insurance, term life provides no cash value accumulation, meaning policyholders gain no financial return if they outlive the term. Premiums can also increase significantly upon renewal, potentially becoming unaffordable.

Additionally, coverage ends after the term, leaving individuals unprotected when they may need it most. These limitations highlight the importance of carefully evaluating long-term financial goals before choosing term life insurance as a permanent solution.

Bga Insurance Life Insurance

Bga Insurance Life InsuranceDrawbacks Of Term Life Insurance

Term life insurance is often praised for its affordability and simplicity, making it an attractive option for individuals seeking temporary coverage at a low cost. However, like any financial product, it comes with notable shortcomings that potential policyholders should carefully consider.

While term life insurance provides a death benefit for a specified period—usually between 10 and 30 years—it does not offer lifelong protection or any cash value accumulation. Once the term expires, coverage ends unless the policy is renewed or converted, often at significantly higher premiums.

This lack of long-term security and investment component can be a major disadvantage, particularly for those who outlive their term or require permanent protection. Furthermore, individuals may mistakenly assume that their needs will remain static, only to find themselves without coverage when they need it most.

Lack of Cash Value Accumulation

One of the most significant disadvantages of term life insurance is that it does not build cash value over time.

Can Someone With Cancer Get Life Insurance

Can Someone With Cancer Get Life InsuranceUnlike permanent life insurance policies such as whole or universal life, which include a savings or investment component, term life is purely insurance coverage with no opportunity for financial growth. This means that if you cancel the policy or outlive the term, you receive no return on your premiums. All the money paid into the policy is retained by the insurer unless a claim is filed during the active term.

For individuals interested in combining life insurance with an asset-building component, the absence of cash value makes term life a less strategic financial tool, even though it remains cost-effective for pure protection.

Temporary Coverage With No Lifelong Protection

Term life insurance is designed to provide coverage for a limited period, which inherently means it may not protect you for your entire life. If you purchase a 20-year term policy at age 35, the coverage will expire when you are 55. Should you pass away one day after the term ends, your beneficiaries will not receive the death benefit.

This temporary nature makes term life unsuitable for individuals concerned about covering end-of-life expenses, such as funeral costs or estate taxes, later in life. While some policies offer conversion options to permanent insurance, these often come with strict time limits and medical underwriting requirements, making lifelong protection uncertain and potentially more expensive if delayed.

Can You Put A Life Insurance Policy In A Trust

Can You Put A Life Insurance Policy In A TrustWhen a term life insurance policy expires, continuing coverage typically requires either renewing the existing policy or applying for a new one—both of which come with increased costs. Renewal premiums are often based on your attained age, meaning that rates can skyrocket as you grow older.

For example, premiums at age 60 can be several times higher than those at age 40 for the same death benefit. Additionally, if health conditions develop during the term, reapplying may result in denied coverage or even higher rates due to increased risk. This pricing structure can make long-term reliance on term insurance financially impractical, especially for individuals whose insurance needs extend beyond the initial term.

| Drawback | Description | Impact on Policyholder |

|---|---|---|

| No Cash Value | Term policies do not accumulate savings or investment component. | Policyholders gain no financial return if they outlive the term. |

| Temporary Coverage | Coverage ends after the specified term (e.g., 10, 20, 30 years). | Risk of being unprotected in later years when needs may persist. |

| Higher Renewal Premiums | Rates increase significantly upon renewal due to age and health changes. | Long-term affordability is compromised, especially after age 50. |

Drawbacks of Term Life Insurance: What You Should Know

What are the key drawbacks of term life insurance policies?

Lack of Cash Value Accumulation

Term life insurance policies do not build any cash value over time, which is one of their most significant limitations compared to permanent life insurance options.

This means that if the policyholder outlives the term, there is no financial return on the premiums paid. Unlike whole or universal life insurance, where a portion of the premium contributes to a savings component, term insurance is purely a death benefit protection tool. As a result, it offers no living benefits and cannot be used as a financial asset during the insured's lifetime.

- Term life insurance premiums are paid purely for protection and do not contribute to any investment or savings account.

- Policyholders cannot borrow against the policy or withdraw funds, as there is no cash reserve.

- After the term ends, all previous premium payments are lost if no death benefit is claimed.

Temporary Coverage Duration

Term life insurance provides coverage only for a specified period, such as 10, 20, or 30 years. Once the term expires, the protection ends, leaving the individual uninsured unless they renew or purchase a new policy.

This limited duration may not be sufficient for individuals with long-term financial responsibilities that extend beyond the term, such as ongoing debts, dependents with special needs, or estate planning objectives. Renewing the policy often comes with substantially higher premiums due to increased age and potential health decline.

- After the term ends, coverage stops unless actively renewed, which requires another round of underwriting.

- Extending coverage into older age is possible but often cost-prohibitive due to age-related premium increases.

- There is no guarantee of future insurability, meaning health issues could prevent renewal or new policy acquisition.

Increasing Costs Upon Renewal

When a term life insurance policy reaches its expiration, renewing it typically results in significantly higher premiums.

Since rates are often based on the insured’s age at the time of renewal, a 20-year term ending when the policyholder is 60 will reflect much higher rates than when they first purchased the policy at age 40. Additionally, conversion options—switching to a permanent policy—may be available but often come with complex terms and elevated costs. This makes long-term financial planning harder, as future expenses are uncertain.

- Renewal premiums are recalculated based on the insured’s current age, leading to steep cost increases.

- Even minor health changes can further elevate renewal rates or limit options.

- Conversion to permanent insurance may preserve some original underwriting, but the resulting policy is usually more expensive than newly purchased term coverage.

Is term life insurance a bad choice due to its limitations?

What Are the Main Limitations of Term Life Insurance?

Term life insurance is often criticized for specific restrictions that may not suit every individual’s long-term financial planning. One key limitation is its temporary nature—coverage only lasts for a set term, such as 10, 20, or 30 years, after which the policy expires with no payout if the insured is still alive.

This means that if the policyholder outlives the term, they receive no financial return despite decades of premium payments. Another significant drawback is the lack of cash value accumulation; unlike permanent life insurance, term life does not build equity or savings that can be borrowed against or withdrawn.

As a result, policyholders cannot use it as a financial asset during their lifetime. Renewing a term policy after expiration often comes with substantially higher premiums due to increased age and health risk, making long-term coverage potentially unaffordable.

- The coverage duration is fixed and non-permanent, limiting its usefulness beyond the selected term.

- There is no cash value or investment component, meaning no opportunity for wealth accumulation.

- Renewal premiums can rise sharply, especially if health has declined, making continued coverage expensive.

When Is Term Life Insurance a Practical Option?

Despite its limitations, term life insurance can be a strategic and cost-effective solution in several life stages or financial scenarios.

For young families, it provides essential protection at an affordable rate during years of high financial responsibility, such as mortgage payments and children’s education costs. Its lower premiums compared to permanent insurance allow individuals to obtain higher death benefits for the same cost, maximizing financial protection when it’s needed most.

Term life is also suitable for temporary needs, like covering a business loan or ensuring income replacement during working years. Since most claims on term policies are paid out only if death occurs during the active term—aligning with periods of peak financial dependency—it remains a logical fit for many consumers seeking simple, focused protection.

- It offers affordable, high-coverage protection during critical financial obligation periods.

- It aligns well with time-bound liabilities like mortgages, student loans, or child-rearing expenses.

- It enables budget-conscious individuals to prioritize essential coverage without paying for added features.

How Do Alternatives to Term Life Insurance Compare?

Permanent life insurance policies, such as whole life or universal life, offer features that address some of term insurance’s limitations, but come with trade-offs. These alternatives provide lifelong coverage and include a cash value component that grows over time and can be accessed through loans or withdrawals. This makes them function partially as both insurance and investment vehicles.

However, the premiums for permanent policies are significantly higher—often five to fifteen times more than term policies with similar death benefits. This cost difference can limit the amount of coverage a person can afford, potentially reducing the effectiveness of their financial safety net.

Additionally, the investment returns within permanent policies may be modest after fees, and surrender charges can erode early cash value gains. For many, the extra cost may not justify the benefits unless estate planning, legacy goals, or lifelong dependents are central concerns.

- Permanent policies offer lifelong coverage and cash value, but at a much higher premium cost.

- The investment component in permanent insurance may underperform compared to independent investment strategies.

- High fees and complexity make permanent insurance less transparent and potentially less efficient for basic protection needs.

Frequently Asked Questions

What happens if I outlive my term life insurance policy?

If you outlive your term life insurance policy, the coverage simply ends, and no death benefit is paid. You receive nothing back unless you have a return-of-premium rider, which refunds your payments. This can be a drawback if you've paid premiums for years but gain no financial benefit, especially if your needs extend beyond the term.

Does term life insurance build cash value?

No, term life insurance does not build cash value. Unlike permanent life insurance, it provides pure death benefit protection for a set period. This means there’s no savings component or investment growth. While this keeps premiums lower, it also means you can’t borrow against the policy or access funds during your lifetime, which may limit financial flexibility.

Yes, premiums can increase significantly if you renew the policy after the initial term expires. Most term policies have level premiums during the term, but once it ends, rates are based on your age and health at renewal. This can make coverage unaffordable later in life, especially if health declines, which is a major disadvantage compared to locked-in permanent insurance rates.

Is term life insurance suitable for long-term financial planning?

Term life insurance may not be ideal for long-term financial planning since coverage ends after a set period. If you still need protection when the term expires, obtaining new coverage can be costly or impossible due to age or health issues. It's best for temporary needs like income replacement or mortgage protection, not for lifelong estate or inheritance planning.

Leave a Reply