Indexed Universal Life Insurance Law Firm

Indexed Universal Life (IUL) insurance offers a unique blend of life coverage and potential cash value growth tied to market indexes.

However, its complexity often leads to misunderstandings, mismanagement, or even legal disputes. When policyholders face issues such as inadequate disclosures, misleading sales practices, or denied claims, the need for specialized legal expertise becomes critical.

A law firm focused on Indexed Universal Life insurance provides essential guidance and representation in navigating these intricate matters. These legal professionals understand the nuances of insurance contracts, regulatory requirements, and policyholder rights, ensuring clients receive informed advocacy and pursue rightful remedies when necessary.

Columbia Indexed Universal Life Insurance Law Firm

Columbia Indexed Universal Life Insurance Law FirmUnderstanding Indexed Universal Life Insurance: The Role of a Specialized Law Firm

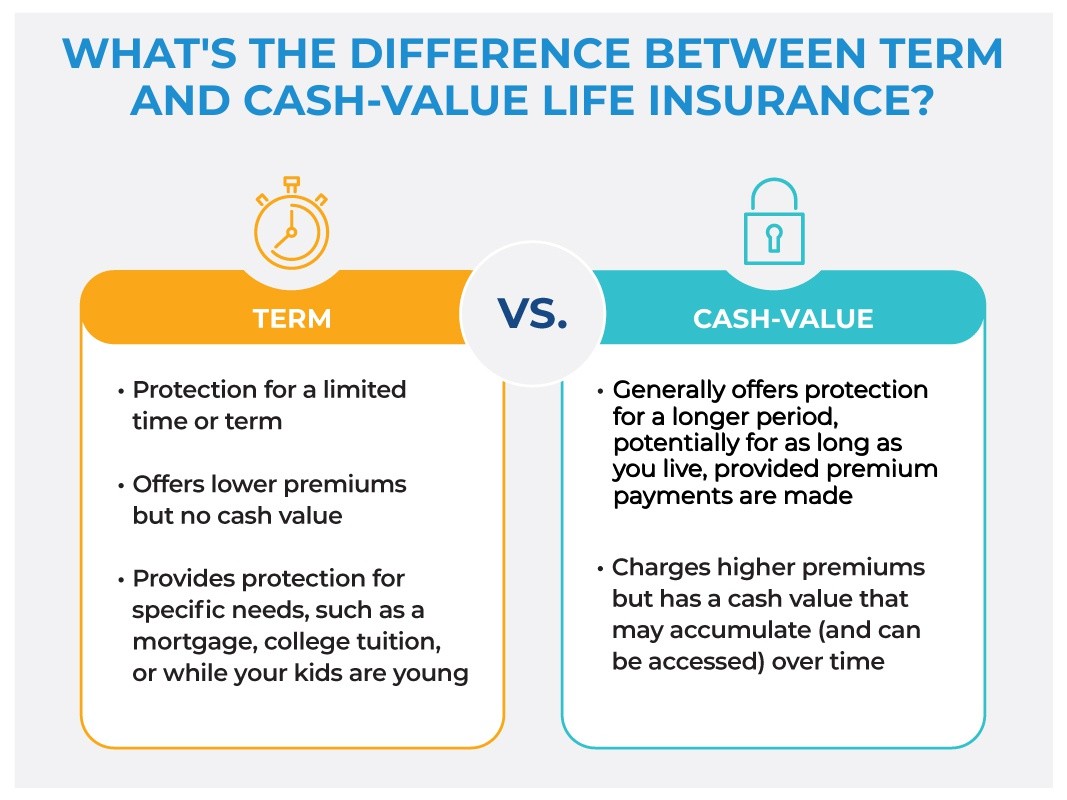

Indexed Universal Life (IUL) insurance is a complex financial product that combines a death benefit with a cash value component tied to a market index, such as the S&P 500.

While IUL policies offer potential for growth and tax advantages, they also come with intricate terms, caps, participation rates, and fees that can lead to disputes, misrepresentation, or underperformance. When policyholders believe they’ve been misled during the sales process or are experiencing issues with their policy performance, benefits, or claims, they often turn to an Indexed Universal Life Insurance Law Firm for legal guidance.

These specialized firms focus on holding insurance companies accountable, investigating sales practices, and representing clients in arbitrations, litigation, or regulatory complaints. With deep knowledge of insurance law and financial regulations, these attorneys help policyholders understand their rights and pursue compensation when policies fail to perform as promised.

Common Legal Issues with Indexed Universal Life Insurance Policies

Policyholders frequently encounter legal challenges related to misrepresentation, churning, excessive premiums, and unsuitability when it comes to Indexed Universal Life Insurance.

Best Life Insurance Without 2 Year Waiting Period

Best Life Insurance Without 2 Year Waiting PeriodAgents may overstate potential returns, fail to disclose significant fees or surrender charges, or recommend IUL policies to individuals for whom they are not financially appropriate—such as seniors relying on fixed incomes. In many cases, beneficiaries or policyholders only discover the problems years later when the cash value fails to grow as projected or when unexpected premium demands jeopardize the policy’s viability.

A specialized IUL law firm investigates these claims by reviewing sales records, agent disclosures, and policy illustrations to determine whether regulatory violations or breaches of fiduciary duty occurred.

How an IUL Insurance Law Firm Can Help You Seek Justice

An Indexed Universal Life Insurance Law Firm offers critical support to individuals harmed by deceptive or negligent insurance practices.

These legal teams conduct comprehensive case evaluations, gather supporting documentation, and work with financial experts to reconstruct policy performance based on actual versus projected outcomes. They often file claims with FINRA arbitration or state insurance departments when misconduct by brokers or financial advisors is evident.

New York Life Insurance Company Brokerage General Agency Imo

New York Life Insurance Company Brokerage General Agency ImoIn many cases, clients recover substantial compensation through settlements or awards, covering lost premiums, reduced cash values, and emotional distress. Because statutes of limitations apply, timely consultation with an experienced IUL attorney is essential to preserve legal rights and maximize recovery potential.

Choosing the Right Law Firm for Your IUL Insurance Claim

Selecting a law firm with specific experience in Indexed Universal Life Insurance disputes is vital, as these cases require understanding both insurance law and financial product complexities. Look for firms that exclusively or primarily handle insurance-related litigation and have a track record of successful client outcomes.

Transparency in communication, access to in-house financial analysts, and experience with major insurance carriers such as Nationwide, Pacific Life, and Lincoln Financial are strong indicators of capability. Many reputable firms offer free consultations and work on a contingency fee basis, meaning you pay nothing unless they recover compensation on your behalf.

| Aspect | Key Considerations | Why It Matters |

|---|---|---|

| Legal Expertise | Firm specializes in IUL or life insurance litigation | General practitioners may lack the financial insight needed for complex policy disputes |

| Case Evaluation | Offers free, no-obligation review of your policy | Helps determine if misrepresentation or misconduct occurred without upfront cost |

| Fee Structure | Works on contingency—no fee unless compensation is recovered | Reduces financial risk for policyholders pursuing justice |

| Industry Experience | History of handling cases against major insurers | Proven ability to challenge powerful insurance companies |

| Client Support | Provides clear communication and regular updates | Ensures you remain informed throughout the legal process |

Understanding Indexed Universal Life Insurance: Legal Guidance and Compliance

What is the top law firm specializing in Indexed Universal Life (IUL) insurance policies?

Online Life Insurance Prices

Online Life Insurance PricesWhat Makes a Law Firm a Leader in Indexed Universal Life (IUL) Insurance Policy Cases?

- A top law firm specializing in Indexed Universal Life (IUL) insurance policies is distinguished by its deep understanding of insurance law, financial products regulation, and fiduciary duty violations. These firms typically have extensive experience litigating disputes involving misrepresentation, unsuitable sales practices, and agent misconduct related to IUL products.

- Such law firms often work with financial experts and actuaries to analyze policy performance, projections, and illustrations provided by insurance agents to determine whether clients were misled about potential returns or risks. This technical analysis is critical in building a strong legal case against insurers or distributors.

- Additionally, leading firms maintain a national or multi-state practice, allowing them to represent policyholders across jurisdictions and handle complex cases involving major insurance carriers such as Nationwide, Pacific Life, or Lincoln Financial.

Are There Law Firms Specifically Known for Handling IUL Insurance Disputes?

- While no single law firm is universally recognized as the top firm for IUL cases, several boutique litigation firms and insurance-focused practices have earned strong reputations. Firms like Barrasso Usdin Kupperman Freeman & Sarver, LLC in New Orleans and Diamond McCarthy LLP have handled significant insurance bad faith and misrepresentation litigation, including cases involving complex life insurance products.

- Other notable firms include Nik Solicitors and The Law Offices of David L. Baugh, which have publicly represented clients in disputes over IUL policy suitability, premium miscalculations, and misleading sales practices. These firms often publish analyses or speak at industry events on the risks associated with IUL products.

- Many of these firms operate on a contingency fee basis, enabling policyholders to pursue legal action without upfront costs. Their success often comes from aggregating similar claims or pursuing class-action-like strategies against insurers who used standardized, deceptive sales tactics.

What Legal Issues Arise with Indexed Universal Life Insurance Policies?

- IUL policies frequently lead to legal disputes due to the complexity of their structure, particularly regarding indexed crediting strategies, cap rates, participation rates, and inherent fees. Policyholders often claim they were not adequately informed about how these components could limit growth or increase premium requirements over time.

- Common allegations include churning (excessive policy replacement), failure to disclose risks, and recommending IUL policies to retirees or low-risk clients for whom such products are unsuitable. These issues fall under securities and insurance regulatory frameworks, including FINRA and state insurance department guidelines.

- Another significant legal concern is the use of exaggerated illustrations showing high returns based on historical index performance, which may not account for fees, caps, or market volatility. Courts have ruled such illustrations can constitute misrepresentation when they create unrealistic expectations about policy performance.

What are the legal and financial drawbacks of Indexed Universal Life (IUL) insurance?

Complexity and Misunderstanding of Policy Mechanics

- Indexed Universal Life (IUL) insurance is often criticized for its intricate structure, which combines a death benefit with a cash value component linked to a market index, such as the S&P 500. This complexity can lead to significant misunderstanding among policyholders about how the cash value actually grows, especially since it does not directly participate in the stock market but instead uses index performance to determine interest credits.

- The mechanisms like caps, participation rates, and spreads limit the amount of index gains credited to the policy, and these terms are often not clearly communicated to consumers. As a result, policyholders may overestimate potential returns, believing their cash value will grow in line with market gains when, in reality, the effective interest credited is frequently much lower.

- This lack of transparency and consumer awareness opens the door to legal disputes, especially if agents fail to provide a comprehensive IUL illustration or do not adequately explain assumptions. Regulators have taken action against insurers and agents for misleading sales practices, which can result in legal liabilities and regulatory scrutiny.

High Costs and Fees Impacting Long-Term Performance

- IUL policies come with substantial costs, including premium loads, cost of insurance (COI) charges, administrative fees, and rider fees, all of which can erode the cash value growth significantly over time. These expenses are often front-loaded, meaning the greatest deductions occur in the early years of the policy, reducing the compounding effect crucial to long-term growth.

- Because the cost of insurance increases with age, the required premium to keep the policy in force may rise substantially in later years. If the cash value does not grow as projected due to lower-than-expected index performance or fee overruns, the policy may lapse unless the policyholder injects additional funds, creating a financial burden.

- Additionally, the financial projections provided during the sale are often based on optimistic scenarios involving high index performance and low expenses, which rarely materialize in practice. When actual performance falls short, policyholders may discover too late that their IUL is underperforming or unsustainable, potentially leading to financial losses and legal claims for misrepresentation.

Tax and Regulatory Risks with Potential Legal Exposure

- One of the primary attractions of IUL is its tax-deferred growth and tax-free withdrawals or loans, but this benefit is contingent on the policy qualifying as life insurance under IRS guidelines. If the cash value grows too quickly relative to the death benefit, the policy may fail the IRS’s definition of life insurance and become reclassified as a Modified Endowment Contract (MEC), eliminating many favorable tax treatments.

- MEC classification means that withdrawals are taxed on a last-in, first-out (LIFO) basis, making them partially taxable, and policy loans may no longer be tax-free. This creates unexpected tax liabilities for policyholders who believed they had structured a tax-advantaged financial strategy.

- From a legal perspective, if agents or financial advisors do not adequately warn clients about MEC risks or structure policies aggressively to boost early cash value growth, they may face liability for negligence or breach of fiduciary duty. Regulatory bodies like FINRA and state insurance departments monitor such practices closely, and non-compliance can result in fines, sanctions, or litigation.

What happens to the cash value in an IUL policy upon the insured's death under life insurance laws?

How Death Benefits Are Distributed in an IUL Policy

When the insured person passes away, the primary function of an Indexed Universal Life (IUL) insurance policy is to pay out the death benefit to the designated beneficiaries. This death benefit is typically a predetermined amount specified in the policy and is generally income-tax-free under current U.S. life insurance laws.

The cash value that has accumulated within the IUL policy does not get paid out separately to the beneficiaries. Instead, once the death benefit is issued, the insurance company absorbs the existing cash value. In essence, the death benefit replaces the cash value, and no additional payments are made based on the internal savings component. The distribution process usually begins after the beneficiary files a claim and submits a certified death certificate.

- The beneficiary submits a death claim to the insurance carrier, including required documentation.

- The insurer processes the claim and verifies policy status and entitlement.

- Upon approval, the full death benefit is issued, typically within a few weeks, and the policy terminates.

Fate of Accumulated Cash Value at the Time of Death

The cash value in an IUL policy, which grows based on the performance of a selected stock market index (with a floor to prevent losses in downturns), ceases to exist as a separate asset upon the insured’s death.

This means that while the policyholder may have contributed premiums over time—some funding the death benefit and some accumulating as cash value—the entire cash value is effectively extinguished when the death benefit is paid.

The beneficiaries do not receive both the death benefit and the cash value; they only receive the death benefit. This structure is by design, as life insurance policies are intended to provide a lump sum to beneficiaries upon death, not to function as dual-purpose savings and insurance vehicles for heirs.

- The cash value stops accruing interest or index-based gains the moment the insured passes away.

- The insurer uses any remaining cash value to offset the cost of providing the death benefit.

- Beneficiaries have no access to the cash value after the death benefit is disbursed.

Impact of Policy Loans and Withdrawals on Death Benefits

If the policyholder took loans or withdrawals against the cash value during their lifetime, this can directly affect the final death benefit amount received by the beneficiary.

Any outstanding loan balance, including accrued interest, is typically deducted from the death benefit before payment. For example, if the death benefit is $500,000 and there is an unpaid loan of $50,000 with $5,000 in interest, the beneficiary would receive $445,000.

It’s important to note that even though the cash value may have been partially depleted by such transactions, the reduction in the death benefit is what ultimately impacts the beneficiary. Policyholders can minimize this impact by repaying loans or adjusting premium payments to maintain sufficient cash value.

- Unpaid policy loans reduce the net death benefit available to beneficiaries.

- Interest on outstanding loans continues to accrue until the insured's death.

- Strategic loan management during the policyholder’s lifetime can help preserve the intended death benefit.

Frequently Asked Questions

What is Indexed Universal Life Insurance?

Indexed Universal Life (IUL) insurance is a type of permanent life insurance that offers both a death benefit and a cash value component. The cash value grows based on the performance of a stock market index, like the S&P 500, without direct market exposure. It provides flexibility in premiums and potential tax-deferred growth, making it a strategic option for long-term financial planning and wealth accumulation.

How can an IUL law firm help me?

An IUL law firm specializes in the legal and regulatory aspects of Indexed Universal Life insurance policies. They assist with policy reviews, compliance issues, disputes with insurers, and estate planning integration. These firms ensure your policy aligns with current laws and protect your rights as a policyholder. Their expertise is valuable in maximizing benefits while minimizing legal and financial risks associated with complex insurance products.

Are there tax benefits with Indexed Universal Life insurance?

Yes, Indexed Universal Life insurance offers several tax advantages. The cash value grows tax-deferred, and policyholders can access funds through tax-free loans or withdrawals, under IRS rules. Additionally, the death benefit is typically paid to beneficiaries free of income tax. These benefits make IUL a powerful tool for tax-efficient wealth transfer and retirement planning, especially when structured properly with guidance from experienced legal and financial professionals.

What should I consider before purchasing an IUL policy?

Before purchasing an IUL policy, consider your financial goals, risk tolerance, and long-term commitment to premium payments. Understand the fees, caps, and participation rates affecting cash value growth. Consult with a knowledgeable IUL law firm to review policy terms, ensure compliance, and evaluate how the policy fits within your estate plan. Proper due diligence helps avoid future disputes and ensures the policy performs as intended over time.

Leave a Reply